Separating the Issues in the Cedar Falls Mining Debate

After reviewing the Planning & Zoning meeting from March 25th, 2026 where Bitcoin minnig, Zoning and a new CFU powerplant wer dicussed, it’s clear that several different issues were being discussed at the same time. When those get mixed together, it becomes difficult to evaluate the project clearly.

I think it helps to separate the discussion into four distinct categories.

1. Zoning & Land Use

This is the most important and most durable question.

Concerns about noise, building type (containers vs. permanent structures), water systems, and proximity to neighborhoods all fall into this category. These are not Bitcoin-specific issues — they apply to any industrial use.

If the concern is that this site should not be rezoned from light industrial to heavy industrial, that’s a legitimate argument. It sets precedent and affects long-term land use decisions for the city.

2. Power Plant

There are also concerns tied to the new power plant itself — environmental impact, scale, and whether it should be built at all.

That’s a separate policy decision.

If the concern is emissions or the role of a peaker plant, those questions should be addressed directly:

When does the plant run?

What is the cost of running it versus buying power from the grid?

How often is it expected to operate?

Those are important questions, but they are not inherently tied to Bitcoin mining.

3. Governance & Process

Some of the strongest concerns raised were about process and oversight.

The city, CFU, and the applicant are closely connected, which raises reasonable questions:

Is there sufficient independent review?

Has there been a third-party analysis of costs, noise, and environmental impact?

These are solvable issues:

Independent studies

Clear contract structures

Ongoing monitoring and transparency

4. Utility Economics (Where Bitcoin Actually Enters the Picture)

Only at this stage does Bitcoin mining itself become relevant.

CFU described miners as an interruptible load:

They consume electricity when it is cheap and abundant

They shut off when prices spike or the grid is stressed

This matters because utilities buy electricity at varying prices. If a flexible customer uses low-cost energy and avoids high-cost periods, it can reduce the utility’s average cost of power.

As one CFU representative explained, this dynamic lowers the average cost of power by reducing the need to purchase expensive electricity during peak periods.

That doesn’t guarantee lower bills, but it does suggest that mining — when structured correctly — is not inherently a cost burden and may improve system efficiency.

A Simple Test

One question that helps clarify the discussion:

If this facility were in a fully enclosed building, met all noise standards, and used a closed-loop system — would there still be strong opposition?

If the answer is yes, then the issue may not be the impacts themselves, but the perception of Bitcoin.

Closing Thought

There are legitimate concerns in this discussion, particularly around zoning, noise, and long-term planning. But many of the arguments raised in the meeting were not aligned with how the system was actually described.

If this decision is going to be made well, it should be grounded in:

Bitcoin Is Good for the World. Here’s the Case Most People Miss.

The typical Bitcoin conversation goes like this: someone brings it up, someone else calls it a scam or an environmental disaster, and the conversation collapses into noise before anything interesting gets said. What gets lost in all that noise is that Bitcoin is quietly doing things that genuinely matter — things that have nothing to do with the price chart. Specifically:

What Bitcoin mining is doing to stabilize the power grid

What it’s doing to reduce emissions in the atmosphere

What Bitcoin is doing to subsidize the creation of green energy assets (solar, wind, hydro)

What it’s doing for people living under governments that would rather they had no financial options at all

The Grid Problem Nobody Talks About

Here’s something that doesn’t get enough attention: the modern electric grid has a flexibility problem. Renewable energy sources like wind and solar are intermittent by nature. The wind doesn’t blow on command. The sun doesn’t shine at peak demand. So grids end up with these awkward mismatches — too much power when nobody needs it, not enough when everyone does.

The traditional fix involves “peaker plants” — gas-burning facilities that sit idle most of the time and fire up when demand spikes. They’re expensive to build and costly to run.

Bitcoin miners are different.

Unlike most industrial loads, they can scale down quickly when the grid is stressed and ramp back up when surplus power returns. That makes them one of the few large energy buyers that can absorb excess power without demanding constant priority from the grid.

That matters because electricity demand in the U.S. is rising again, driven by AI data centers, manufacturing, and electrification. Traditional data centers require continuous power and add stress at exactly the wrong times.

Bitcoin mining is the opposite.

It soaks up energy when the grid has too much and steps back when the grid needs relief.

It doesn’t just consume electricity — it makes the system more flexible.

And this isn’t just theoretical.

At a recent city council discussion in Cedar Falls, Iowa, the local utility (CFU) explained that their Bitcoin mining partner actually helps lower electricity costs for residents.

Their reasoning was simple:

The miner uses excess power when it’s cheap

It shuts down when power is expensive

That reduces the utility’s need to buy high-cost electricity

As one CFU representative put it during the meeting (timestamp 2:05:57):

“That lowers the average cost of power because we’re buying a lot less.”

It’s not true that Bitcoin miners automatically raise electricity prices.

It depends entirely on how the contracts are structured.

In Cedar Falls, the utility itself is saying the opposite:

👉 The miner helps lower average costs for residents.

That’s not a theory.

That’s happening in practice.

The Methane Story Is Even More Interesting

If you’ve heard that Bitcoin is bad for the environment, you’ve probably heard the energy consumption number. What you likely haven’t heard is what Bitcoin mining can do with one of the most potent greenhouse gases on the planet: methane.

When oil is drilled, natural gas often comes up with it. In places where there’s no pipeline infrastructure nearby, operators may vent it or flare it. Both are bad outcomes. Methane has a much stronger warming effect than CO₂, and imperfect flaring leaves a meaningful share unburned.

Instead of releasing methane, it gets destroyed — and turned into useful energy.

Bitcoin doesn’t just use energy — it can clean up wasted energy.

Bitcoin Is Quietly Funding the Green Energy Build-Out

This is the angle that almost never makes it into mainstream coverage, and it’s arguably the most important one for long-term climate outcomes.

Building a renewable energy project is expensive and financially risky. One of the toughest windows is the period after the project is capable of generating electricity but before it is fully interconnected and earning reliable revenue from the grid.

During that phase:

Energy is being produced

But there may be no reliable buyer

That’s a problem.

A Cornell-led study published in ACS Sustainable Chemistry & Engineering found that Bitcoin mining can materially improve project economics during this phase. In Texas alone:

In parts of Texas, electricity prices can go negative.

Why?

Too much power

Not enough transmission

Not enough local demand

When that happens, producers may be forced to:

👉 Sell electricity at a loss 👉 Or shut down production

One West Texas solar plant had to sell 10.1% of its energy at a loss because of this.

Bitcoin mining changes that.

Instead of dumping excess energy into an oversupplied market, the plant can redirect that power into mining — creating a buyer of last resort and a price floor for surplus energy.

In that case, adding Bitcoin mining increased total site revenue by 3.7%.

Most people in the developed world think of money as a neutral tool. But in many countries, financial systems are instruments of surveillance and control.

Every serious objection to Bitcoin has already been thought through — and answered. This is a challenge to critics to find one that hasn’t.

2026 · A challenge to skeptics · Not financial advice

“The root problem with conventional currency is all the trust that’s required to make it work.”

— Satoshi Nakamoto, 2009

What Is Honest Money?

Money, at its core, is a technology for storing and transferring value across time and space. For thousands of years humans have searched for a form of money that couldn’t be corrupted — that couldn’t be debased by kings, inflated away by central banks, or confiscated by governments with printing presses and good intentions.

Gold came closest. Fixed supply. Scarce. No one could create more by decree. But gold has real problems — it’s heavy, hard to divide, difficult to verify, and nearly impossible to transmit across borders without trusting intermediaries. The very institutions gold was meant to protect us from ended up holding it for us. And once they held it, they printed paper on top of it. And once they printed paper, they removed the gold backing entirely.

Bitcoin is the first monetary technology in human history that combines the scarcity of gold with the transmissibility of the internet — and does so without requiring trust in any institution, government, or person. That is what makes it honest money. The rules are in the code. The code is public. No one can change the supply schedule. No one can freeze your coins without your keys. No one can print more.

Fixed supply of 21 million coins. Predictable issuance schedule. Decentralized — no single point of control or failure. Permissionless — no one can deny you access. Censorship resistant — no one can stop a valid transaction. Verifiable — anyone can audit the entire system.

Bitcoin as Money: The State of Adoption Argument

Critics love to point out that Bitcoin fails the three classical tests of money: store of value, medium of exchange, and unit of account. They’re not entirely wrong — yet. But this critique completely ignores that every monetary technology in history went through an adoption curve where these properties emerged gradually.

The dollar wasn’t always trusted. Gold wasn’t always liquid. The internet wasn’t always fast. Pointing at Bitcoin’s current limitations as though they’re permanent is like critiquing the iPhone in 2007 for not having an app store.

The sequence of monetary adoption is predictable and Bitcoin is following it precisely:

Stage 1 — Collectible / Speculation

Early adopters buy it because they believe others will value it later. This is where Bitcoin spent most of its early years. It still has some of this character today but has largely moved beyond it.

As volatility dampens with deeper liquidity and wider adoption, transacting in Bitcoin becomes practical. Layer 2 solutions like Lightning Network are already enabling this. As the price stabilizes at higher levels, the incentive to spend rather than hold increases.

Stage 4 — Unit of Account

Prices denominated in satoshis. This is the final stage and the most distant — but not implausible in a world where Bitcoin has achieved reserve asset status globally.

21MMaximum Supply. Ever.

3-4MEstimated Lost Forever

762KCoins Held by Strategy

$170BUS Spot ETF Assets

Bitcoin as Philosophy

Bitcoin is not just a financial instrument. It is a philosophical statement — arguably the most important one made in the field of money since Bretton Woods.

Distrust of institutions is not paranoia. The 2008 financial crisis demonstrated that the institutions entrusted with the monetary system could be catastrophically wrong, spectacularly rewarded for failure, and bailed out with money created from nothing. The genesis block was not subtle about this. Satoshi embedded a newspaper headline about bank bailouts directly into Bitcoin’s first block.

Sovereignty over your own wealth is a human right. The ability to hold value that cannot be confiscated, frozen, or inflated away without your consent is not a radical idea. It is the natural extension of property rights. Bitcoin makes that right technologically enforceable for the first time in history.

Scarcity is not the enemy of prosperity. The dominant monetary philosophy of the 20th century held that money supply should be managed. Bitcoin rejects this entirely. Its scarcity is not a bug but the central feature. Scarcity is what gives money its meaning as a store of value across time.

Rules over rulers. Perhaps the deepest philosophical claim Bitcoin makes is that mathematical rules enforced by cryptography are more trustworthy than any human institution. Not because humans are evil — but because humans are fallible, corruptible, and mortal. Code, once deployed and sufficiently decentralized, is not.

The Environmental Argument — Already Answered

Bitcoin uses an enormous amount of energy. This is true. What critics leave out is what kind of energy, and what Bitcoin does with it.

Bitcoin miners are uniquely flexible electricity consumers — they can be switched on and off instantly, making them ideal buyers of stranded and curtailed renewable energy that would otherwise be wasted. Wind farms and solar arrays frequently produce more power than grids can absorb. Bitcoin absorbs the excess, making previously uneconomic renewable projects viable.

More compellingly: Bitcoin miners are increasingly deployed to combust methane — the gas vented from oil wells and landfills that would otherwise enter the atmosphere directly. Methane is roughly 80 times more potent as a greenhouse gas than CO2 over a 20-year period. Using it to mine Bitcoin converts it to CO2, dramatically reducing net emissions. This is not spin. It is chemistry and thermodynamics.

The environmental argument against Bitcoin is a legacy talking point that has not kept pace with how mining has actually evolved. The narrative persists not because it is accurate but because it is politically useful to those with incentives to undermine Bitcoin’s legitimacy.

The Objections — And Why They’ve Been Answered

What follows is an honest accounting of the most serious objections to Bitcoin, and the responses that Bitcoin thinkers have developed over 17 years of adversarial scrutiny. These are the actual strongest arguments — tested against people who have spent careers trying to find the fatal flaw.

Objection: Quantum Computing Will Break Bitcoin’s Cryptography

A sufficiently powerful quantum computer could theoretically derive private keys from public keys, compromising holdings.

Quantum computing is an existential threat to every cryptographic system on earth — every bank, every government database, every secure communication. Bitcoin is actually among the more adaptable systems since it can hard fork to quantum-resistant algorithms, which already exist and are being standardized. This objection proves too much — if quantum breaks Bitcoin, it breaks everything.

Objection: Transaction Fees Can’t Sustain Miner Security After Halvings

Block rewards halve every four years until ~2140. At zero issuance, miners must be compensated by fees alone. If fees are insufficient, hash rate drops and the network becomes vulnerable.

This objection ignores the difficulty adjustment — one of Bitcoin’s most elegant mechanisms. If hash rate drops, difficulty adjusts down, making mining profitable again at a new equilibrium. At $1 million per coin, even tiny fees in BTC terms are substantial in dollar terms. The security budget concern disappears at scale.

Objection: A Superior Competitor Will Replace Bitcoin

Technology has network effects that shift. Something better could emerge and Bitcoin could become MySpace.

This analogy fundamentally misunderstands monetary network effects. MySpace lost to Facebook because Facebook was more useful in ways users could immediately feel. Monetary network effects are far stickier — the value of money IS the network. Gold held its monetary premium for 5,000 years. Bitcoin may have crossed a similar threshold.

Objection: Governments Will Ban It

Sovereign monetary authorities will not permit a parallel monetary system to challenge their control.

China has “banned” Bitcoin multiple times. It still trades in China. Bans on information and mathematics don’t work. More importantly, the US regulatory posture has reversed dramatically. Spot ETFs are approved. SAB 121 has been rescinded. Institutional banks can now custody digital assets. The world’s largest capital market is opening, not closing.

Objection: Bitcoin Is Too Volatile To Be Money

Something that drops 70% in a year cannot function as a reliable store of value.

Volatility is a function of market depth and adoption, not an intrinsic property of Bitcoin. Every asset becomes less volatile as liquidity deepens. Gold was volatile when its market was thin. Bitcoin’s volatility has been declining measurably each cycle as institutional participation deepens. This objection describes the present state and projects it as permanent — a logical error.

The Real Challenge

After seventeen years of adversarial scrutiny by some of the sharpest minds in cryptography, economics, and computer science — every major objection to Bitcoin has been examined and answered.

The honest answer to “what could derail Bitcoin?” is the unknown unknown — the thing no one has thought of yet. That’s intellectually serious. That’s the right answer.

The challenge to skeptics is simple: find a serious objection that the Bitcoin community hasn’t already examined in depth and answered.

Even Fidelity — one of the world’s largest asset managers — has concluded that ignoring Bitcoin is no longer a prudent approach. The burden of proof has shifted. It is no longer on Bitcoin advocates to justify owning it — it is on skeptics to justify owning zero.

Most people who try to find a fatal flaw end up owning Bitcoin instead.

The Structural Buying Pressure Nobody Is Talking About

Beyond the philosophical and technical case, there is a mechanical reality forming in markets that deserves attention. Fidelity’s 2026 research finds that Bitcoin has delivered the highest risk-adjusted returns of any asset class over both five and ten year horizons — and that even a 1-3% allocation has historically produced meaningful portfolio improvements.

Companies like Strategy have pioneered a model where corporate balance sheets treat Bitcoin as a primary treasury reserve asset, funding ongoing purchases through equity and non-margin debt instruments. Strategy alone holds over 762,000 coins — more than 3.6% of the total supply — and has structured its balance sheet specifically to avoid any forced liquidation scenario. This is a one-way accumulation machine.

This is happening simultaneously with the halving-driven supply reduction — the programmatic 50% reduction in new Bitcoin issuance that occurs every four years. Less new supply entering the market. More institutional demand absorbing existing supply. ETFs holding billions on behalf of pension funds, endowments, and retail investors who will never touch a private key.

These forces compound. They do not reverse without a fundamental change in the thesis — and the thesis has only gotten stronger with time.

The Honest Remaining Risks

Intellectual honesty requires acknowledging what is genuinely uncertain.

The unknown unknown. Bitcoin could fail in ways no one has conceived. This is true of any system. It is taken seriously precisely because it cannot be dismissed — but also cannot be acted upon. You cannot hedge against what you cannot imagine.

A catastrophic BIP. The Bitcoin Improvement Proposal process is the mechanism by which protocol changes are proposed and adopted. Conservative governance makes bad changes unlikely — but not impossible. The community’s demonstrated ability to resist even well-intentioned changes (the block size wars) suggests this risk is managed, not eliminated.

Partial success. The most likely “disappointing” outcome is not failure but incomplete success — Bitcoin becomes a globally recognized store of value held by institutions and sovereigns, reaching prices that would have seemed absurd a decade ago, but never fully displacing fiat as the unit of account for everyday life. This would be an extraordinary outcome for holders while representing a partial failure of the original vision.

Conclusion: The Game Theory of Honest Money

You don’t have to believe Bitcoin will succeed to understand why it might.

A small number of people who deeply understand the monetary system, the history of currency debasement, and the technical properties of Bitcoin will continue to accumulate. Their accumulation drives price. Rising price attracts attention. Attention drives adoption. Adoption deepens liquidity. Deeper liquidity dampens volatility. Dampened volatility enables broader use as money. Broader use as money drives further adoption.

The masses don’t need to understand sound money theory for this to play out. They never do. They didn’t understand TCP/IP to use the internet. They didn’t understand double-entry bookkeeping to trust banks. They will not need to understand elliptic curve cryptography to hold Bitcoin.

History doesn’t require universal understanding to move in a direction. It requires enough people who understand to make it inevitable for everyone else.

The question is not whether Bitcoin is perfect. No monetary system is. The question is whether it is more honest than what we have — and whether honest money, once available, can ultimately lose to dishonest money in a world where information moves freely.

If you’ve found a flaw the Bitcoin community hasn’t already answered, the world is listening.

This essay represents the author’s analysis and philosophical perspective. It is not financial advice. Bitcoin is a volatile asset. Past performance does not guarantee future results. Do your own research. Hold your own keys.

For years, the standard framework for retirement income has been the 4% rule.

The idea is simple: if you want $48,500 per year of spending, you would typically need roughly:

$48,500 × 25 = $1,212,500

In other words, about $1.2 million invested in a diversified portfolio to sustainably withdraw that income.

But recently I came across an interesting thought experiment involving two relatively new preferred securities.

Before diving into the math, it’s important to note that these securities ultimately sit within financial structures connected to Bitcoin, so they carry some exposure to the long-term success of Bitcoin itself. More on that later.

Two High-Yield Preferred Securities

Two securities caught my attention:

Strategy Series C Preferred (STRC) – currently yielding about 11.5%

Strive Asset Management Preferred (SATA) – currently yielding about 12.75%

Both are preferred securities issued by companies building financial products around Bitcoin treasury strategies.

An interesting feature is their dividend timing.

STRC has an ex-dividend date around the 15th of the month

SATA has an ex-dividend date around the 28th of the month

The actual cash payment arrives roughly 15 days later, but what matters for dividend eligibility is simply holding the shares on the ex-dividend date.

After that date passes, an investor can sell the shares and still receive the dividend.

The Rotation Idea

Because the ex-dividend dates occur at different times of the month, a strategy some investors discuss is rotating between the two securities:

Hold STRC through its ex-dividend date (~15th)

After the ex-date passes, sell and move into SATA

Hold SATA through its ex-dividend date (~28th)

Then rotate back to STRC and repeat

In theory, this rotation attempts to capture both dividend streams each month.

The Yield Math

Using approximate yields:

SATA: 12.75% STRC: 11.5%

Combined:

12.75% + 11.5% = 24.25%

If an investor pays roughly 24% tax on the income:

24.25% × 0.76 ≈ 18.4% after tax

That’d give this investor $18,400 per a year income on $100k or $36,400 per a year on $200k.

The Early Retirement Thought Experiment

Suppose an early retired investor allocated $200,000 to this strategy.

At a 24.25% gross yield, the income would be:

$200,000 × 0.2425 = $48,500 per year

Under the traditional 4% rule, producing that same income would require:

$48,500 × 25 = $1,212,500

So the comparison looks like this:

Strategy

Capital Required

Traditional 4% rule

~$1.2 million

Preferred rotation idea

~$200,000

That’s roughly a 6× difference in required capital.

Even More Interesting for Early Retirees

For some early retirees who structure their income carefully, qualified dividend income can fall within the 0% federal tax bracket.

In that scenario, the full 24.25% yield could theoretically flow through without federal income tax.

Using the same $200,000 example:

Investment

Yield

Annual Income

$200,000

24.25%

$48,500

That level of income could cover a meaningful portion of living expenses for many households.

The Bitcoin Connection

It’s important to understand what ultimately sits underneath these securities.

Both STRC and SATA are part of financial structures built around companies holding significant amounts of Bitcoin on their balance sheets.

At the base of these preferred securities is therefore some degree of Bitcoin risk.

If Bitcoin were to fail as an asset class entirely, the underlying business models supporting these preferreds would likely fail as well.

However, if Bitcoin continues to grow and remain valuable over time, these structures should continue to function as designed.

It is also possible that as demand for these types of securities increases, the dividend yields could gradually decline. Markets tend to compress yields when large numbers of investors compete for the same income-producing assets.

So the yields discussed above should be viewed as the current state of the market, not necessarily a permanent condition.

Finally there is company risk. Strive (ASST) issues SATA and Strategy (MSTR) issues STRC. Either company could fail for some generic business reason and that woudl also be a risk, just like any business.

Final Thoughts

For decades, the 4% rule has been a useful guideline for thinking about retirement income.

But financial markets are constantly evolving, and new structures occasionally appear that change the math in interesting ways.

This rotation idea may or may not prove durable over the long run. But it highlights how emerging financial instruments—especially those tied to Bitcoin treasury strategies—are beginning to create entirely new types of income assets.

And sometimes, when you run the numbers, it’s worth pausing and asking:

Could the future of income investing look different than the past?

As of 3-16-2026 I started an account to do this specifically. I will share the results in a few months or at the end of the year to see how it’s gone and if anything has changed since I started this experiment.

All prices in the below table are per share. multiple the # shares x any price to get the total amount. I started with 10x $97.22 = $972.20 and a purchase of 10 shares of SATA. I borrowed money for this experiment from a HELOC at a rate of 6.25% starting.

4-9-2026 I borrowed another $1k and purchased $2k of STRC. As of this date my current plan is to work up to $12k invested with this test.

$12k x (.1275+.115) = $2,910/year in dividends.

$2910x 22% tax = $640.20 in taxes

$12,000 x 6.25% interest loan = $750

$2910-$750-640.20 = $1,519.80/year income. If i have to make 4 trades (2x/month + 2x sell/month) x 12 months = 48 trades/year, if the trades each toook 1 hour, which they ceratinly do NOT, but hypotentically $1,519.80/48 = $31.66/hour, if you wanted to compare this back to a wage job. Since it’s completely borrowed money and not my standard cash I think this is useful comparison to determine if this is worth the time. This also scales more $/hr with more money as the amount of time to trade 100k shares vs 10 shares should be the same. As the market matures I will continue to learn more about this.

None of this takes into account buying STRD every 3rd month instead of STRC to get a 3 month quarterly payout vs the monthly STRC payout. I will be doing that in June 2026 and keeping track of that data here also. That should significatinly improve all the metrics, in theory. Adding STRD every 3rd months will hypothetically add 13% return to the total plan. But you have to subtract 1/4 of the 11.5% since you are missing a monthly STRC payout so 11.5%/4 = 2.875% so 13% – 2.875% ~ 10% added on top. So at $12k/year x 10% = $1,200 which is about as much as the total previous plan! adding that in

the same loan applies though $12,000 x 6.25% interest loan = $750

so $4,110-$904.20-$750 = $2455.80 vs $1,519.80 for a total final increase of $936 / $12k =7.8% real improvement. and $2455.80/48 hrs = $51.16 /hr.

We will see in 12 months if this is working!

$12k also makes sense for me as it is <1% of my net worth. So I wouldn’t be in a catastropic position if this failed. Risk/reward should be considered for anyone doing anything like this. Do your own research. Not Financial advice.

Proposing to Pay STRC Dividends Semi-Monthly Strategy is proposing to pay semi-monthly dividends on STRC, instead of monthly. If approved and adopted, we believe this would lead to reduced reinvestment lag, enhanced liquidity, market efficiency, and increased price stability.

Proposed Amendment Timeline April 17: Preliminary Proxy Filed April 28: Definitive Proxy Filed(1) Voting Opens June 8: Meeting Date Voting Completes June 30: First Record Date under New Cadence(2) July 15: First Payment Date under New Cadence(2)

STRC is planning to pay 2x / month. This would be good for the stability of STRC. But it would make it harder to do this strategy of moving between the 2 stocks, STRC and STRD each month.

Also in the month of April my purchase of STRC (20 shares) happened at $100/share but selling was $99.50 for a loss of $0.50/share. The dividend should be $0.96/share for a profit of $0.46 but that is still a lot below the goal. We will see in a couple days how this plays out. SATA is also discussing going to semi monthly payouts. If both were doing semi monthly on alternating weeks it might still allow the rotation but with 2x the work. The price might be more stable. I will continue this experiment for some time further.

5-14-2026 – SATA (Strive) has come out with the plan to pay DAILY dividends. This is a huge idea but also negates this rotation strategy. I will hearby cancel this rotation strategy for these dividends. It seems it wasn’t particualry successful since the stocks were falling and not quite recovering during the time needed to buy back for the next stock.

STRIVE – The Daily Dividend Company

Digital Credit is going DAILY

Below are the improvements on the horizon for $SATA and @Strive

Understanding Ponzi schemes, Bitcoin carry trades, and how new financial instruments are evolving

Recently there has been a wave of posts online claiming that MicroStrategy and securities like STRC are “Ponzi schemes.”

That claim misunderstands both what a Ponzi scheme actually is and how these instruments work.

Before labeling something a Ponzi scheme, it helps to start with a clear definition.

What Is a Ponzi Scheme?

A Ponzi scheme is a fraudulent investment structure where:

Investors are promised returns

Those returns are not generated by real economic activity

Early investors are paid using money from new investors

The scheme collapses once new inflows stop

The defining characteristics are:

No real underlying asset

No productive activity generating returns

Fabricated account statements or hidden losses

Mathematical collapse once new money stops coming in

The most famous example is Bernie Madoff, who fabricated account balances while paying existing investors with money from new clients.

If there is no real asset and no real economic activity, you may be looking at a Ponzi scheme.

An Interesting Contrast: Social Security

Ironically, one of the closest structures many Americans participate in that resembles a Ponzi-style payment system is **Social Security Administration’s Social Security program.

Social Security works by:

taxing current workers

using those taxes to pay current retirees

There is no large invested pool backing the system. Instead, it relies on a continuous stream of new contributors to fund previous participants.

Government projections show the trust funds are expected to become depleted within the next decade, after which benefits would have to be reduced or taxes increased to maintain payouts.

This is not fraud — it is a demographic funding system created by law — but it illustrates an important point:

Money flowing from new participants to previous participants does not automatically make something a Ponzi scheme.

A Ponzi scheme specifically requires deception and fake returns.

Now let’s look at MicroStrategy.

What MicroStrategy Actually Does

MicroStrategy is a publicly traded company that:

issues equity and debt securities

uses the proceeds to purchase Bitcoin

holds that Bitcoin on its balance sheet

The underlying asset is Bitcoin, which is publicly verifiable on the blockchain.

Investors buying MicroStrategy securities know exactly what they are purchasing.

Nothing is hidden. Nothing is fabricated. The underlying asset exists and can be independently verified.

You may disagree with the strategy.

But it clearly does not meet the definition of a Ponzi scheme.

What STRC Actually Is

STRC is a preferred stock issued by MicroStrategy that pays a monthly dividend currently around 11.5% annually.

The capital raised from selling STRC is used to purchase additional Bitcoin.

Conceptually, the structure resembles a carry trade.

A Bitcoin Carry Trade

For decades global investors used the Yen carry trade.

The strategy worked like this:

Borrow Japanese yen at extremely low interest rates

Convert yen into higher-yielding assets (often U.S. dollars)

Capture the yield difference

STRC works in a somewhat similar way — but with Bitcoin.

Instead of:

Yen → USD

The structure is effectively:

USD → Bitcoin

Investors provide capital and earn roughly 11.5% yield, while MicroStrategy accumulates Bitcoin.

What the Market Has Actually Shown

STRC began trading in July 2025.

Around August 2025, Bitcoin traded near $120,000.

Since then Bitcoin has experienced significant price volatility.

Yet STRC has generally continued trading near its $100 reference price.

That doesn’t prove the structure will work forever.

But it does show something important:

So far, the instrument has functioned roughly as designed.

Financial markets tend to expose broken structures quickly.

The Lindy Effect

There is a concept known as the Lindy effect.

The Lindy effect suggests:

The longer something survives, the longer it is likely to continue surviving.

We see this with technologies, institutions, and financial instruments.

Gold has survived thousands of years. Stock markets have survived more than a century. Bitcoin itself has now survived multiple boom-bust cycles.

Each month that STRC:

maintains its price near $100

pays its dividend

continues operating normally

…the probability that the structure works increases slightly.

What Are the Real Risks?

None of this means STRC or MicroStrategy are risk-free.

But the risks are often misunderstood.

The real risks are tail risks — low-probability but high-impact events.

For example:

1. Catastrophic failure of Bitcoin

If Bitcoin were somehow fundamentally broken — a critical cryptographic flaw, catastrophic protocol failure, or a coordinated global ban that destroyed liquidity — the entire thesis behind MicroStrategy’s balance sheet would be undermined.

2. Corporate catastrophe unrelated to Bitcoin

Another possibility would be some major event affecting the company itself:

fraud inside the company

regulatory disaster

management misconduct

or some unforeseen corporate collapse

These risks exist for every public company.

3. Extreme financial system disruption

In a severe financial crisis, credit markets can temporarily freeze. Any company that relies on capital markets — including MicroStrategy — could be affected.

Risk Is Not Fraud

The irony in many of these debates is that the word “Ponzi” often gets used as a general insult for anything people don’t understand.

Real Ponzi schemes involve deception, fake assets, and fabricated returns.

MicroStrategy and STRC involve transparent securities backed by a publicly verifiable asset.

Whether someone believes in Bitcoin or not, the structure is visible to everyone.

In fact, one of the broader trends of the past decade has been the opposite of a Ponzi scheme: systems where the underlying asset is more transparent than ever before.

Bitcoin’s supply is public. Bitcoin’s transactions are public. Bitcoin’s monetary policy is fixed.

Financial instruments like STRC are simply new ways that traditional capital markets are interacting with that asset.

You may think the strategy is aggressive. You may think the trade will fail.

But the difference between risk and fraud still matters.

And confusing the two only makes it harder to understand what is actually happening in financial markets today.

Big idea: Spain found a mountain of silver in Bolivia, spent like crazy, stopped building real industries—and the bill came due. The same thing is happening today, just with money printers instead of mines.

1) The mountain

In 1545, Spanish explorers struck the richest silver deposit in history: Cerro Rico, “the rich mountain,” in what’s now Bolivia. A city called Potosí exploded out of the rock. At its height, it was larger than London or Paris. For two centuries, roughly two-thirds of the world’s silver came from that one mountain. Spain looked unstoppable.

2) Easy money, hard problems

So much silver poured into Europe that prices began rising year after year. For nearly a thousand years, prices in Europe had been flat. Then suddenly, everything—from bread to rent—started costing more. Historians call it the Price Revolution.

Spain thought it was getting richer. In reality, its silver was just buying less and less.

3) The addiction loop

Spain borrowed against future silver shipments, funded endless wars, and built palaces to show off its power. Sound familiar? Borrowing against your future is exactly what modern governments do when they run deficits every single year—financing today’s comfort with tomorrow’s labor and taxes. And those “endless wars”? Spain fought them across Europe. The U.S. fights them across the globe. Different century, same playbook.

4) “Free” silver, “free” money

The silver was basically free to Spain—mined with forced labor that cost almost nothing. That “free” flow of money metal fueled reckless spending and inflation.

Today, printing money is even freer. No mines, no ships, no workers—just a digital entry at the central bank. But the result is the same: more money chasing the same goods, rising prices, and wealth concentrating in financial assets instead of productive work.

5) The wage spiral

When silver poured into Spain, mining and trade paid far more than farming or manufacturing. Workers chased the high wages, and everyone else demanded raises to keep up. That wage inflation pushed up local costs across the board.

It soon became cheaper to buy foreign goods than to make them at home. English and Dutch craftsmen could undersell Spanish products even after shipping them across the sea. Local factories and farms couldn’t compete. Spain’s economy drifted from production to consumption—spending instead of building.

You can see the same thing happening today. Money printing and easy credit inflate salaries in finance, tech, and government while driving up housing, energy, and labor costs everywhere else. Manufacturing can’t keep up, so we import the difference. The result? A strong currency, cheap goods, and a shrinking middle class.

6) The next chapter — Japan

What if the next Spain isn’t America yet—but Japan? As this interview with macro analyst Roberto Rios explains, Japan is further down the same path: zero interest rates, quantitative easing, and government debt so large that the central bank must choose between saving its currency or saving its bond market.

For decades, Japan has printed money to prop up its financial system, even buying stocks outright to keep prices from falling. That free liquidity created an illusion of stability—until inflation returned and the yen began collapsing. Now Japan faces the impossible choice every over-leveraged empire eventually faces: protect the currency and crash the system, or print the money and destroy the currency.

It’s the same dilemma America is approaching, just delayed by our global reserve-currency privilege. The “free silver” of the 1500s became “free paper” in the 1900s and “free digital dollars” in the 2000s. The pattern never changed—only the technology did.

7) The simple lesson

Resources aren’t wealth. Printing money isn’t wealth. Making things is wealth. When prosperity feels “free,” it’s usually borrowed from the future.

8) Today’s echo

Easy credit. Quantitative easing. Deficit spending. Each promises painless prosperity—more liquidity, more growth, no trade-offs. But it’s the same story Spain wrote 500 years ago: short-term abundance, long-term decay.

Spain’s “free” silver built an empire that rotted from within. Japan’s “free” money is imploding quietly. And America’s “free” dollar is next in line—just with better branding and digital ink instead of metal.

9) Bitcoin and the Dollar Endgame

What if Japan’s collapsing bond market isn’t just a regional crisis but a preview of America’s financial future?

In the Bitcoin for Millennials episode, host Bram talks with macro analyst Roberto Rios (“Peruvian Bool”), who has been tracking this “dollar endgame” for years. While most people fixate on Bitcoin’s short-term price swings, Rios zooms out to the structural problem: every central bank is trapped between saving its currency or saving its bond market. Japan is simply the first to hit the wall.

He calls this dynamic financial gravity—the idea that once debt and money creation expand far enough, gravity pulls everything toward a neutral asset that can’t be printed.

Rios’s core argument:

The global monetary system has reached a point where debt can never shrink; it can only be monetized.

Central banks will print until confidence breaks.

When trust in both sides of the fiat balance sheet—bonds and currencies—collapses, capital will flee into something outside the system entirely.

That’s where Bitcoin enters the picture.

While central banks and institutions still view gold as the “neutral” reserve, Rios argues Bitcoin is the superior version of gold:

Borderless and digital—no vaults, shipping, or intermediaries.

Immune to political capture or forced demand (“fiat” in the literal let-there-be sense).

As he puts it, the Japanese bond crisis could actually trigger the biggest Bitcoin bull run ever. Once Japan’s carry trade unwinds and the yen weakens further, global liquidity shocks will push central banks to print again—reviving the same inflation loop that began with Spain’s silver. Each cycle of monetary rescue drives more people to seek an exit from the system itself.

From silver to paper to code: Spain’s “free” silver created Europe’s first inflation. Japan’s “free” money is collapsing under its own weight. Bitcoin is the gravity well everything eventually falls into.

A common fear I hear about Bitcoin goes something like this: “If it becomes so valuable in the future, people will never spend it. They’ll just hoard it forever — and that means it can’t work as money.”

But let’s pause. That argument assumes that money needs to lose value in order to be useful — that people will only spend if their savings are constantly melting. Does that really make sense?

People Already Save

In reality, people save no matter what. Even with inflationary dollars, households and businesses don’t spend every cent. They put money aside — but because the dollar steadily loses value, they are forced to search for other stores of value:

Stocks

Bonds

Real estate

Gold

Collectibles

This isn’t a feature. It’s a problem. The constant need to escape a leaky dollar creates bubbles, misallocates capital, and makes financial life complicated for everyone.

Take housing, for example. When money loses value, homes become more than shelter — they turn into financial assets. People don’t just buy houses to live in them; they buy them as inflation hedges. That means families looking for a roof over their heads end up competing with investors and savers desperate to preserve wealth. Prices get bid up far beyond the utility value of the home, making affordability worse and turning what should be a basic necessity into a speculative storehouse for capital.

Deflationary Money Doesn’t Paralyze Spending

Critics imagine that if money gains value over time, nobody will use it. But people already spend under deflationary conditions — technology proves this. Everyone knows next year’s phone or TV will be cheaper and better, yet they still buy today. Why? Because they value the use and enjoyment now, not just later.

The same applies to Bitcoin. Once mature, it will likely appreciate at roughly the rate of productivity growth (similar to a low-yield bond). People will hold it to store value — and still spend it when a purchase is worth more than waiting.

Flipping the Narrative

Inflationary money forces people into risky, complex alternatives just to save. Hard money that holds or grows its value removes those distortions. Contrary to the fear, deflationary money won’t break the economy — it may actually fix many of the problems caused by inflationary systems.

And here’s the real irony: many critics already suspect Bitcoin could become extremely valuable — that’s why they worry no one will spend it. But at the same time, they refuse to buy any today. They recognize the upside, but fear keeps them paralyzed on the sidelines.

Conclusion

In a Bitcoin world, homes could go back to being homes, not savings accounts. People could save without speculation, spend without fear of losing purchasing power, and invest in businesses for growth rather than sheltering from inflation. That’s not “useless money.” That’s money finally doing its job.

When we talk about taxes in America, the debate often gets sloppy. People use “income” and “wealth” almost interchangeably, but they’re very different things.

Income is the flow of money earned each year — wages from a job, dividends, or realized capital gains.

Wealth is the stock of assets someone already owns — businesses, real estate, stocks, Bitcoin, etc.

Our tax system is built mainly on income, not wealth. And when commentators conflate the two, it clouds the conversation about fairness and policy.

Income Snapshot

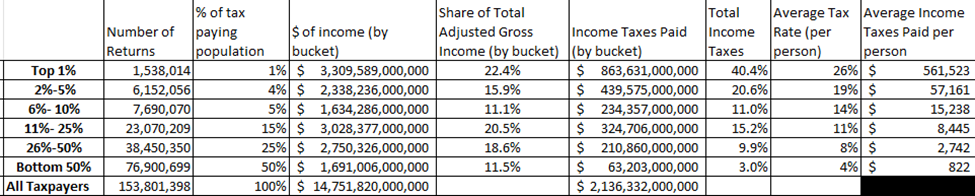

In 2022, the U.S. collected $2.1 trillion in federal income taxes on about $14.8 trillion in total income. That’s about 14.4% of taxable income.

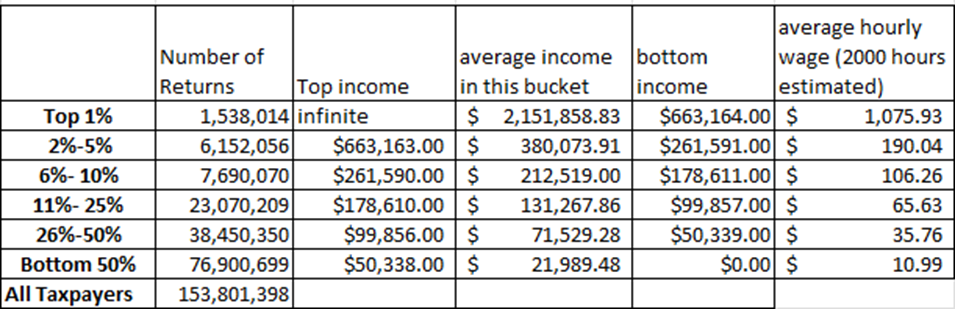

Divide that income across all 153 million taxpayers, and the average income comes out to $95,915, or about $47.96 per hour assuming 2,000 hours of work per year. Of course, averages can mislead — the distribution is anything but equal.

The Top 1%

To qualify for the top 1% in 2022, you needed at least $663,164 of income. On average, these 1.5 million taxpayers earned $2.1 million each.

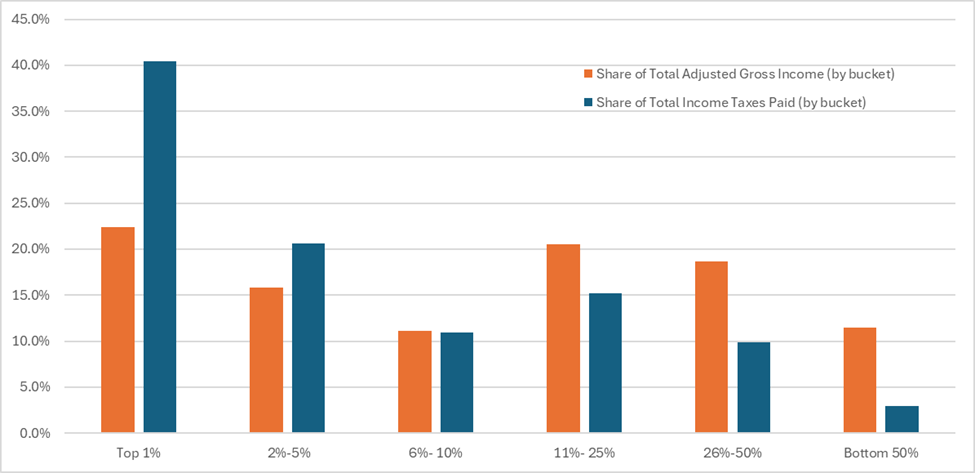

Share of income: 22.4%

Share of taxes paid: 40.4%

Effective tax rate: 26%

The Bottom 50%

The bottom half — about 76 million taxpayers — earned less than $50,339 per year. Their average income was just $21,000, totaling $1.7 trillion across the group.

Effective tax rate: ~4%

Many pay no federal income tax at all, often due to credits like the Earned Income Tax Credit (EITC) or child tax credits.

Wealth Snapshot

If we shift from income to wealth, the picture looks even starker. As of mid-2025, U.S. billionaires hold over $6.2 trillion in wealth, spread across only about 813–867 individuals.

But here’s the catch: the U.S. government is adding about $2 trillion in deficit spending every year. Even if you taxed billionaires at extremely high rates, it might cover only a year or two of deficits. After that, the wealth pool would shrink — and most billionaires would likely relocate to avoid such aggressive taxation.

That doesn’t mean we shouldn’t debate fairness, redistribution, or even wealth taxes. But it does mean we need to be realistic about the math.

Why This Matters

The key takeaway is that income and wealth are different conversations. Most tax debates focus on income flows, yet the loudest arguments are often about wealth concentration. If we mix those together, we miss the real tradeoffs.

I’m happy to debate how much each group should earn, or whether a wealth tax makes sense (though I personally think it doesn’t). But if we want an honest conversation, we have to separate what we’re actually measuring.

Because when we ask, “Who should pay more?” the first step is being clear: are we talking about annual income, or about the stock of wealth built up over decades?

You will notice myd ata is slightly different than from the website. The website continually aggregates so their “top 5%” data includes all the income & people from the top 1% + the 2%-5%. I have broken it down so you can see how much income is in each bucket. I think my method is much more useful. It also allows you to see how much income, taxes, average income, is in each bucket.

When the data is aggregated it always is skewed due to the higher amount of income above it.

You Were So Close: Where the Anti-Empire Analysis Misses Bitcoin’s Role as the Fix

A year old video titled Geo-Strategy #3: How Empire is Destroying America delivers a sharp, compelling critique of the United States’ transformation from a productive manufacturing economy into a hollowed-out empire addicted to easy money, foreign capital, and speculative finance. The lecturer nails several things before they happened:

Trump won

The U.S. dropped bombs on Iran (June 21, 2025).

Empire—not capitalism alone—is the real structural disease.

So far, so good.

But here’s where it falls short: when it comes to solutions, the analysis stops at nostalgia. It groups Bitcoin in with the broader financialized, speculative mindset of the current era—instead of recognizing it as the clearest path out of the collapsing fiat-imperial system.

What the Video Gets Right

1. The Shift to Financialization Was a Disaster The U.S. economy went from 40% of profits coming from manufacturing to only 10%. Meanwhile, financial services ballooned to 40% of profits but employ only 5% of the workforce. It’s not a real economy anymore—it’s rent-seeking on a grand scale.

2. Empire Crowds Out Domestic Prosperity As the video rightly says: the U.S. has 800+ overseas bases, trillions in defense spending, and a growing dependency on foreign goods. Meanwhile, infrastructure decays, wages stagnate, and people struggle to own homes.

3. Easy Money Has Warped the Psyche He astutely observes that young people have a speculative mindset. They want to gamble their way to freedom because working hard for 40 years no longer gets you a house or family. The fiat system broke the ladder.

4. Empires Collapse from Hubris Rome did it. So did Britain. The U.S. has reached a point where it can’t imagine losing, but is too bloated and fragile to truly win.

What the Video Misses Entirely

Bitcoin isn’t a symptom of decline. It’s the cure.

Here’s where the logic fails: Bitcoin gets lumped in with real estate speculation, meme stocks, and Wall Street grifting. That’s a category error.

Bitcoin is:

Not tied to Wall Street.

Not controlled by central banks.

Not created through debt.

It is, in fact, everything the empire cannot print, inflate, or manipulate.

If fiat money is what powers the empire’s global dominance and fiscal addiction, then Bitcoin is the tool that cuts the cord. It’s what lets young people store value, opt out of inflation, and build sovereign systems outside elite capture.

The Real Problem: Fiat, Not Just Empire

Let’s go one layer deeper:

Empire needs fiat to fund wars, bailouts, and pensions.

Fiat needs empire to enforce its global dominance (petrodollar system, SWIFT sanctions, military threats).

It’s a closed loop. And Bitcoin breaks it.

Bitcoin is the only monetary system with no central issuer, no forced trust, no inflationary mandate, and no border. It’s not speculative escapism. It’s the foundation for a post-imperial world.

Final Thought

The lecturer in Geo-Strategy #3 is brave and accurate in his breakdown of how empire is destroying America. But like many critics, he sees the collapse clearly yet misses the exit sign flashing in orange behind him: