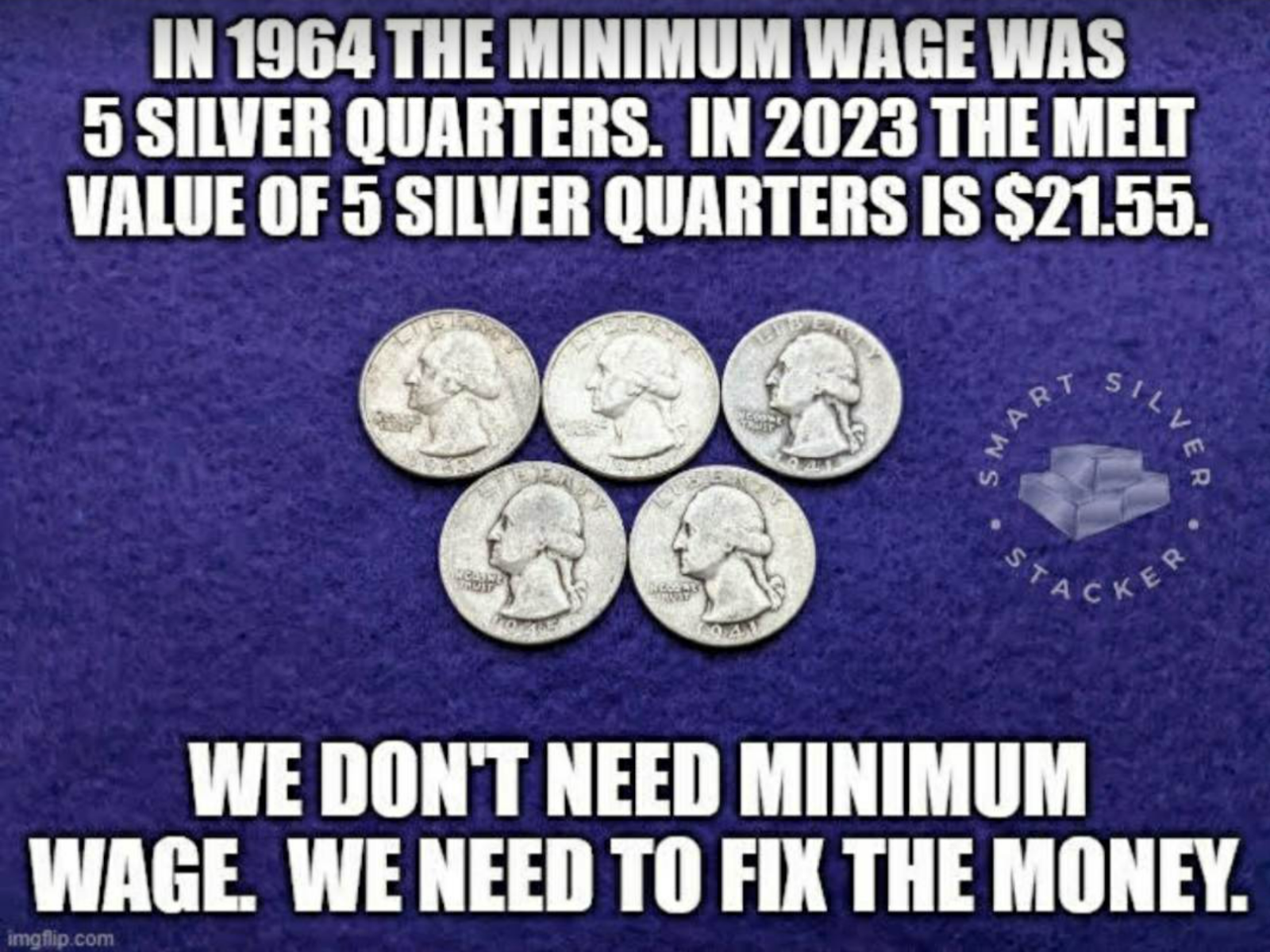

Through 1964 American quarters and dimes were made of 90% silver. Starting in 1965 the inner core is pure copper and the outer covering is copper mixed with nickel. I was discussing this with some friends so I decided to look up some history I recalled about Rome’s debasement of their currency. The first link I found was the below comment and this link to a FEDERAL RESERVE BANK OF ST. LOUIS work book for kids grade 8-12.

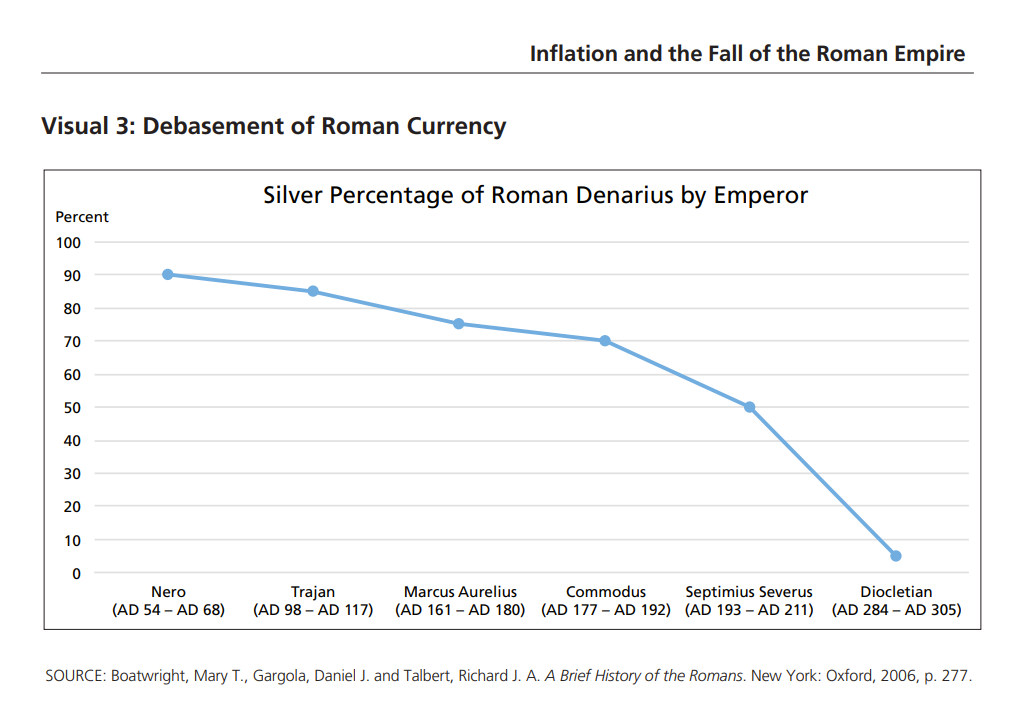

“Commodus (AD 177–AD 192) debased the Roman denarius to about 70 percent silver. Septimius Severus (AD 193–AD 211) debased the Roman denarius to about 50 percent silver. With the added currency, the government could pay for more soldiers and pay existing soldiers more.”

What is incredible is that the Romans “slowly” debased their currency by recalling the money, melting it down and reissuing with a lower percentage of silver. The US government did it quickly by going from 90% to 0% in 1 year! Subsequent dollars were created by adding numbers in the Fed ledger with nothing backing the new money!

Fort Knox holds about 4,580 metric tons of gold which is worth about $250 billion dollars. The US government budget was $6.27 trillion in 2022.

The Government budget deficit in 2022 was $1.38 trillion in 2022.

“A Cantillon effect is a change in relative prices resulting from a change in money supply.” –SWFI

Be Close to the President and Congress

Cantillon also had a theory in which the beneficiaries of the state creating the currency is based on the institutional setup of that state. This essentially means, “he who was close to the king and the wealthy”, likely benefited from the distributional choices of currency through the system. –SWFI

Realizing that the government is constantly creating new money and decreasing the purchasing power of the money you hold in your bank account, what is the average person to do?

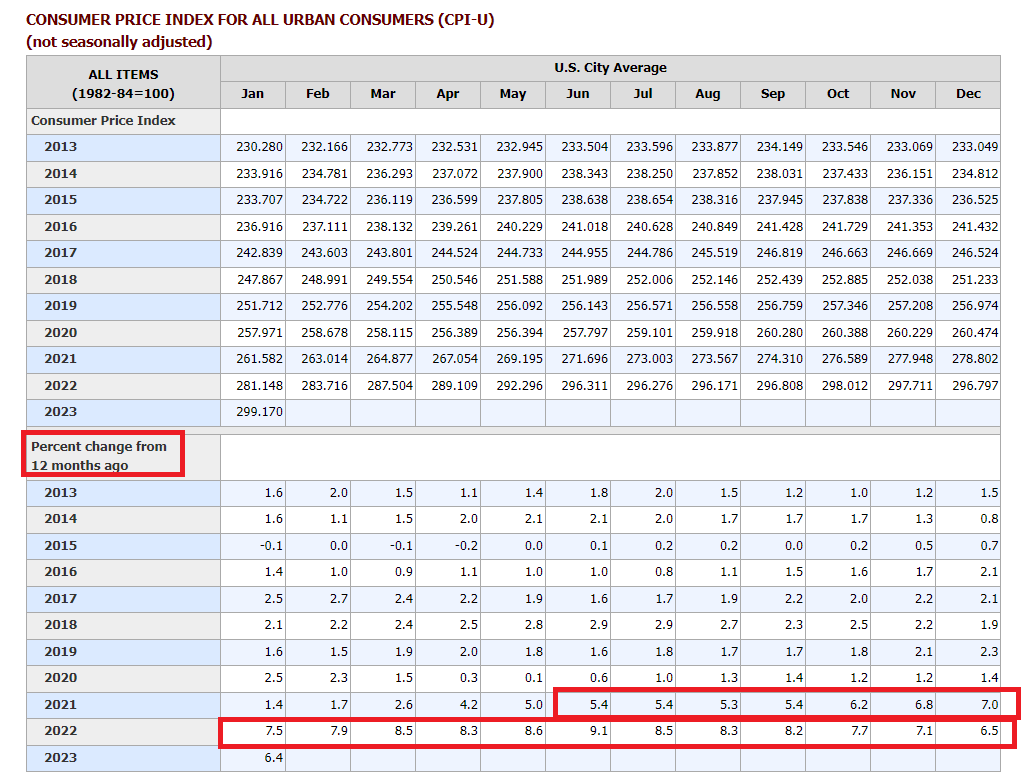

I’ve had more conversations in 2022 and 2023 about “maintaining purchasing power” or “keeping my money from losing value” than ever before in my life, from people who’ve never asked questions like that before. I have to assume it’s because inflation has been between 5%-9% for the past 18 months in the USA, much much higher than the 0%-2% we’ve seen for the previous 10 years and longer.

The answers people are coming up with are the typical ones. I-bonds, which pay interest linked to inflation. A problem with them is you can only put $10,000/year per person into I-bonds.

The next likely targets are either treasury bills or high yield savings accounts. As of today a 180 day treasury bill is paying 4.5%. My personal high yield savings account is paying 4.1%. It’s not worth the extra hassle of buying treasury bills for me personally to get an extra 0.4% yield, but for some people it is. The problem is, with a 6.4% inflation rate over the last 6 months, you are still losing 2% of your purchasing power to inflation, which admittedly is the historic amount people have decided they are “OK” with losing, since the FED inflation target is 2%.

Many people buy real estate and get income from renters each month. Obviously not everyone wants to buy real estate or be a landlord. I have tried it. I am in the process of getting out of it. It wasn’t for me either!

Many people buy stocks as the classic inflation hedge. As we saw last year, stocks can also go down 20% or more in a year. But over long time frames they seem to be the best we have.

Gold is one of the best inflation hedges, over time. I have actually personally considered gold (and to a lesser extent silver) an interesting inflation hedge lately. Like all investing and savings, you need to evaluate the risks and rewards and determine what the right percentage is for each investment relative to your net worth and goals. For me 1% of net worth in gold and silver seems like a safe investment. I wouldn’t say anyone should be 50% or 100% into gold!

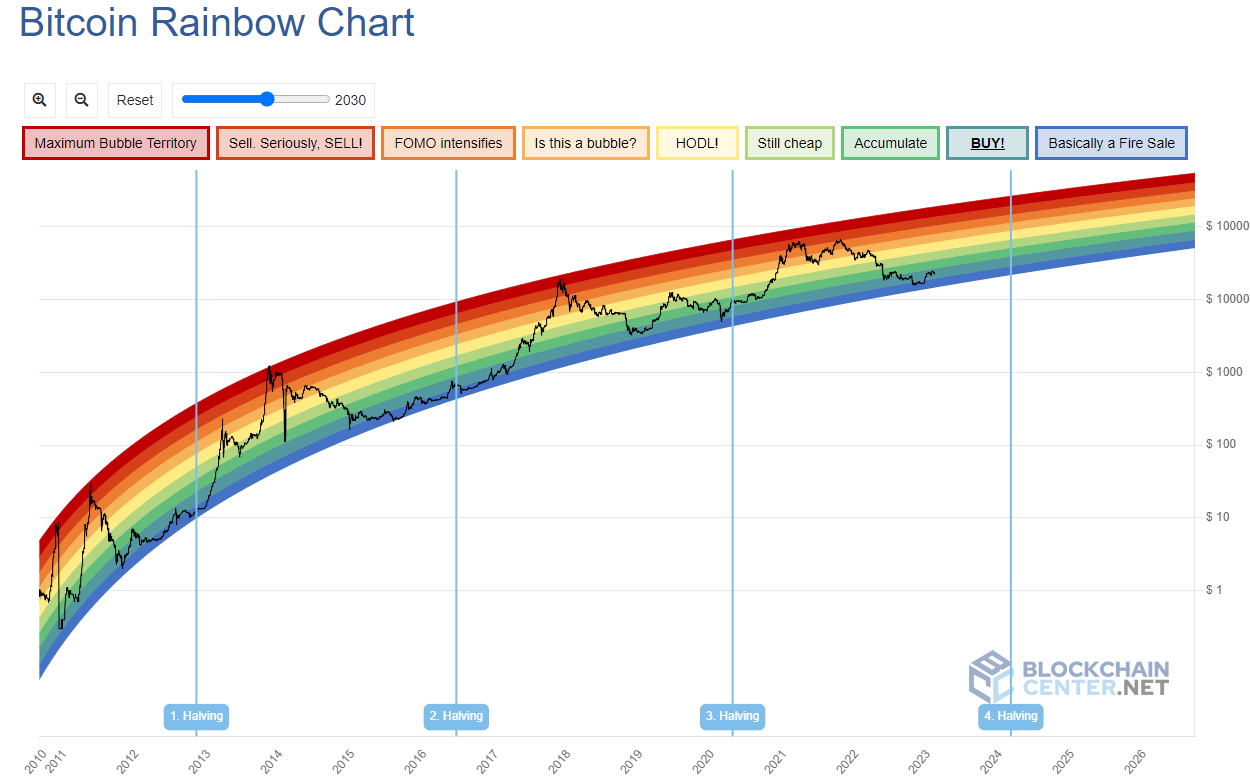

While a lot of these are ways to try to fight inflation there is another new way that might also work. Bitcoin. To me, it seems like a good inflation hedge, in the long term. I can see why many people are hesitant to get into it though. From a high of $69,000 in 2021 it fell all the way down to $15,000 earlier in 2023. It is back up to the low $23,000’s. But for people who just compare to the peak of $69,000 that’s still a long way down. But what people need to remember is, for most any investment, you don’t put every bit of your money in at the peak, usually! I bought some bitcoin for as low as $5,000 in 2018. I bought through the peak and the highest I paid for some bitcoin was $65,000, almost the peak! But that was only maybe $100 worth. I continued buying as it fell all through 2022 and even into the start of 2023. From June-Dec 2022 I bought for less than $20,000 per BTC. So now all that bitcoin is sitting in a profit. While my overall cost basis is about $28,000 and the value is sitting at $23,000, so I am down about 21%. But that is a lot less than the 66% you’d be down if you had bought every coin at the peak of 66%. I think that’s an important lesson for people to learn is that while there are volatile assets, if the asset makes sense, you should still consider allocating a percentage of your net worth towards it. I personally think people should consider 1% of Bitcoin a safe allocation. If you have $50,000 worth of assets that’s only $500. If you lose $500 will you be ruined? Probably not. As with every investment, you should only buy what you plan to keep for 10 years. You also shouldn’t sell when it goes down 50%. In fact you should expect it to go down 50%, whether it’s Bitcoin or stocks.Overall we need to better understand volatility. I believe as more people continue to add their wealth to Bitcoin, $10 at a time, its volatility will reduce and its value will continue to go up. This has already happened over many cycles. As you can see in the bitcoin rainbow chart below. It’s a simple chart tracking the highs and lows of bitcoin.

The best time to get into something is when fewer people are talking about it. A lot of people bought into bitcoin at the peak in 2021 when it was $69,000. That is the exact wrong time to learn about it and buy in because of fear! The best time to buy bitcoin, or anything, is when you have time to buy it and the price isn’t rising dramatically everyday and you get huge FOMO!

In 2017 I bought $100 worth of Bitcoin “just to learn about it”. It took me years to finally get around to learning more about it, as well as the price drastically rising to $40k, to pique my interest. I want to help others learn about it in a calmer state. Learning when it’s at a lower price also gives people a lower cost basis so there is a lot more room to go up! As more people pile into Bitcoin, and adoption is continuing, it will rise. Don’t buy in when the price rises from $40k to $60k in a month. You are already missing out at that point. If you do buy then, don’t be surprised when it falls back to $40k and you are out 50%. You’ve learned the wrong lesson. Start learning now while the price is low. Ask me anything! Start small and slow $50! $10! Good luck!