Here is a link to a video I made about Target Date Funds.

These are great times to be investing! Today is literally the easiest time in all of history to invest. It is also the cheapest time in history to invest. There is an incredible product called a “Target Date Fund” available for “Joe Investor” that is actually a very good tool.

A target date fund is set up to buy thousands of stocks and bonds (diversity) for the owner of the fund. It also automatically transfers more money to bonds (safer) as the fund owner reaches retirement age. This can be the only fund you need in a retirement fund, if you want.

A target date fund usually has a name like 2055 Target Date Fund. Here’s a link to Vanguard Target Retirement 2055 Fund (VFFVX)

There are target date funds available for every 5 years. 2010, 2015, 2020, etc

You can see from the picture below the comparison of the asset allocation of a 2025 vs a 2055 target date fund.

You can see that the 2055 target date fund has a larger percent of stocks, since you will be retiring in the future so you’ll have time to recover from any stock market dips. You can see the 2025 target date fund has a higher percentage of bonds to reduce volatility.

Click below picture to zoom.

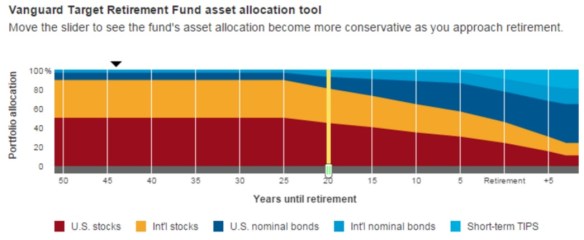

Here is a picture of the path that Vanguard uses to transfer money to bonds as you age.

Here is a link to the Vanguard site where they share more data.

Here is some further reading on if a Target Date Fund is right for your or not.

The pros, cons of using target-date funds in 401(k) plans

5 things you should know about target-date funds

If you want to start investing and have no idea what fund to put your money in, figure out what year target date is available for closest to when you will be 65 and put your money in that fund while you learn a bit more about investing.