In the 1930s, Nazi Germany was broke. The country was reeling from the Great Depression, saddled with war reparations, and shackled by the Treaty of Versailles, which banned it from rearming. Yet within a few years, Germany had built one of the most fearsome war machines in history.

How did they pay for it?

They invented money.

The Mefo Trick

Enter Mefo bills—a financial sleight of hand orchestrated by Hjalmar Schacht, Hitler’s economic wizard and head of the Reichsbank.

The plan was simple and devious:

A fake company called MEFO (Metallurgical Research Corporation) was set up.

MEFO issued IOUs, or “Mefo bills,” to arms manufacturers instead of actual cash.

These IOUs were guaranteed by the German government, and companies could trade them or cash them in later at the Reichsbank.

Crucially, the bills were kept off the official budget, hiding the scale of rearmament.

This created a parallel currency used only within the military-industrial complex. No taxes raised. No gold reserves touched. Just promises backed by more promises.

But there was a catch: each Mefo bill had a five-year maturity. That meant the government had, at most, five years before they had to repay the IOUs in Reichsmarks. The first wave of bills, issued in 1934, would come due in 1939—just as Germany was preparing to invade Poland.

A Booming Mirage

It worked—at first.

Factories roared back to life. Steel, chemicals, and synthetic fuel production surged. Unemployment plummeted. To the outside world, it looked like an economic miracle.

But it wasn’t prosperity—it was military Keynesianism on credit.

By 1938, 20% of German GDP was going to the military. Consumer goods remained scarce. Wages were frozen. Trade unions were banned. Prices were controlled. And Mefo bills kept piling up.

Schacht warned that the system couldn’t last. Eventually, the bills would come due—and the Reichsbank would either default or start printing money. Hitler didn’t care. Instead of slowing down, he pushed harder. Schacht was sidelined, and Hermann Göring took over economic planning with a singular goal: prepare for total war.

War Became the Only Exit

The Mefo system couldn’t sustain itself. Germany was running out of foreign reserves and raw materials. The economy was overheating. The only way out was forward—through invasion, plunder, and conquest.

Occupied countries like Austria, Czechoslovakia, and eventually Poland were stripped of gold, steel, coal, and labor. France was forced to fund the German occupation. The Nazi war machine was now self-financing—by theft.

By the time the Mefo bills started coming due in 1939, the regime began repaying them not through taxes or trade, but by printing money and launching war. The economy was now riding on a tidal wave of credit, conquest, and coercion.

Why It Matters

The Mefo bill scheme shows how financial manipulation can fuel political extremism, militarism, and war. When money is divorced from accountability and markets are warped by ideology, the result isn’t just inflation or inefficiency.

Most of us think of money as the bills in our wallets or numbers in our bank accounts. But money isn’t a physical thing—it’s a system of IOUs. It’s how we track value we’ve created, whether that’s building a fence, baking bread, or writing software.

Here’s the key insight: money itself doesn’t hold value. If it did, you’d want to hoard it. But you don’t. You probably try to get rid of your dollars by putting them into stocks, real estate, or gold—anything to escape inflation.

🧱 A Story About a Fence (and a Broken System)

Imagine this: You build a 100-foot fence for someone. They pay you $100. One year later, you ask them to build a fence for you. They say, “Sure, but now it’ll cost $105.”

Why? Inflation. Your money didn’t hold its value. The effort you gave last year is worth less this year.

And while the U.S. has “low” inflation, other countries—like Argentina—see 100% inflation annually. In places like that, people rush to convert their paychecks into food, bricks, or U.S. dollars just to preserve value.

But let’s be honest: the U.S. dollar and Argentine peso aren’t fundamentally different. Both are government-issued currencies that lose value over time due to overspending and excessive money printing.

⚙️ Enter Bitcoin: Fixed, Transparent, and Decentralized

Bitcoin was designed to fix this exact problem.

There will only ever be 21 million bitcoins.

Each one can be divided into 100 million sats (Satoshis).

Bitcoin is basically a global, digital IOU ledger that nobody controls—but everyone can verify.

Think of it as an open-source Excel spreadsheet that tracks who owns what. But instead of one person controlling it, thousands of computers (nodes) maintain the same list and agree on changes only when a valid transaction is made.

🔨 How Bitcoin Transactions Work

You send a transaction using your app or wallet.

It enters the mempool, a kind of digital waiting room.

Miners select and bundle transactions into a block.

They solve a math puzzle to earn the right to add the block to the chain.

Once added, it’s permanent—and verified by the entire network.

Each block takes about 10 minutes to process. Miners are rewarded with both newly “unlocked” bitcoin (currently 3.125 BTC) and small transaction fees—typically less than 1%, cheaper than credit cards.

🆚 Bitcoin vs “Altcoins”

Bitcoin has no premine, meaning the creator didn’t secretly give themselves coins before anyone else could buy them. Most altcoins (alternative cryptocurrencies) do. That makes many of them less like open money and more like disguised businesses.

Ask yourself: What real problem is this altcoin solving?

The answer is likely that the coin is built around a company structure, because it can’t solve the store of value problem. Bitcoin already solved that problem.

💸 How to Buy Bitcoin Today

Option 1: Brokerages

Buy FBTC, the Fidelity Bitcoin Trust, just like a stock or ETF

Available through Fidelity, Schwab, and others

Small fee: ~0.25% expense ratio

Option 2: Direct Purchase

Use apps like Strike, River, or Cash App

You can hold your own Bitcoin (self-custody) or keep it with the app

📈 Why Bitcoin Could Hit $13 Million

There are $750 trillion in global assets.

Asset Category

Estimated Value (USD)

Real estate

~$360 trillion

Equities (stocks)

~$110 trillion

Bonds (debt markets)

~$135 trillion

Broad money (M2)

~$100 trillion

Gold (above ground)

~$14–15 trillion

Private businesses, art, collectibles, etc.

~$20–30 trillion (est.)

If even $273 trillion of that (stocks, real estate, bonds, money supply) flows into Bitcoin, that’s:

$273 trillion ÷ 21 million BTC = $13 million per coin

This isn’t speculation—it’s about monetary premium, the extra value people add to assets (like real estate or art) just because they don’t trust cash.

Bitcoin is absorbing that value because it’s better money.

🧠 Strategy: It’s Not Too Late

A $10,000 investment today could get you 0.1 BTC. If Bitcoin hits $13 million, that’s worth $1.3 million.

Of course, you shouldn’t invest money you can’t afford to lose. But for many, $10K is a small bet with a big upside.

Bitcoin isn’t just about price—it’s about a fundamentally better way to store and transmit value.

🎯 Final Thought: We’re All Fish in Fiat Water

You’ve lived your whole life in a system where money loses value. It feels normal, but it’s not natural.

Bitcoin is a new kind of money: scarce, digital, decentralized, and global.

Once you understand what money really is, it becomes clear: Bitcoin is not just better money—it’s the future of value itself.

In theory, the ChooseFI and Bitcoin communities should be natural allies. Both value independence, long-term thinking, and building a future that’s not dependent on the whims of politicians or corporations. But in practice, there’s an odd divide: the ChooseFI crowd leans hard into index funds and conventional investing, while Bitcoiners are laser-focused on fixing the money itself.

As someone who walks between both worlds, I think it’s time to bridge this gap.

The ChooseFI Perspective: Smart, but Incomplete

The Financial Independence (FI) movement is one of the best ideas to come out of the last 20 years. It’s a rejection of consumerism and dependence on a 9–5 job. It promotes saving, intentionality, and investing in low-cost index funds to build wealth over time.

But here’s where it falls short: the movement assumes the system is stable enough to invest in indefinitely.

ChooseFI thinkers often acknowledge that inflation erodes purchasing power. That’s why they invest. But they rarely ask why inflation exists or what kind of inflation we’re talking about. They trust the market to keep delivering 7% annual returns because, historically, that’s what it’s done. It’s a comforting narrative—but it’s built on the assumption that the dollar is sound money. It isn’t.

The Bitcoiner’s View: Start With the Root Cause

Bitcoiners take the opposite approach. They start by asking: What if the money itself is broken?

If money is supposed to store value over time and across space, then fiat currency fails that test. Central banks manipulate interest rates and print trillions to bail out markets. This isn’t capitalism—it’s financial engineering.

Bitcoiners understand that if the base layer of the economic system is corrupted, then all the “smart investing strategies” built on top of it are sitting on shaky ground. They argue that if we had sound money—money that couldn’t be debased—then saving would be investing. You wouldn’t have to chase yield to stay ahead of inflation.

In other words, Bitcoin doesn’t replace the FI mindset—it completes it.

The Missed Opportunity

ChooseFI and Bitcoin share the same end goal: personal sovereignty, freedom from wage dependence, and the ability to live life on your own terms. But their tactics differ, mostly because of assumptions they make about the system.

ChooseFI says: “Inflation exists, so invest wisely to beat it.”

Bitcoin says: “Inflation exists because the money is broken—so let’s fix the money.”

Both strategies have value. But only one questions the foundation.

And here’s the deeper issue: too many in the ChooseFI world are afraid to deviate from the script. There’s a culture of “stay the course,” which, while helpful during market turbulence, often becomes a dogma that discourages curiosity. I’ve met people in the FI community who understand something feels off—whether it’s the Fed printing trillions or housing prices going vertical—but they suppress those questions because they fear sounding like conspiracy theorists or rocking the boat.

I want to say this clearly: it’s okay to ask questions. In fact, if you’re pursuing financial independence, you should be asking deeper questions—about the money, the system, and whether the rules we’ve been taught still make sense in a world that’s changing fast.

A Better Future: Combine the Philosophies

Imagine if ChooseFI thinkers began to see Bitcoin not as a speculative gamble, but as a form of saving that aligns with their most cherished values: delayed gratification, personal responsibility, and building a more secure future.

If these two groups came together, we’d have something powerful: a community that not only escapes the rat race—but understands why the race exists, who designed it, and how to stop participating in it altogether.

For ChooseFIers interested in Bitcion I’ll point you to a few of my previous articles below.

In the final week of May 2025, a significant number of companies announced substantial Bitcoin acquisitions, marking a notable trend in corporate cryptocurrency adoption. Below is a list of 20 companies that made headlines with their Bitcoin purchases:

Trump Media & Technology Group (USA)

Investment: Plans to raise $2.5 billion to establish a Bitcoin treasury.

We love to say “just pull yourself up by your bootstraps.” It’s a neat, comforting idea. Work hard, be smart, and success is inevitable.But here’s the truth:

That advice only works if you were born with boots.

In many parts of the world — from Haiti to Senegal to rural India — people aren’t lazy. They’re not stupid. They’re simply locked out of the systems that reward effort.

🌍 Talent Is Universal. Opportunity Is Not.

As economist Ha-Joon Chang points out, people in poor countries are often more entrepreneurial than those in rich ones — because they have to be. There’s no safety net. No trust fund. No stable job waiting after graduation.

But despite this hustle, the game is rigged:

Currencies collapse.

Corruption is common.

Legal systems are slow or predatory.

Borders are closed.

Global capital flows around them, not toward them.

You can be brilliant and still stuck.

👣 Magatte Wade’s Truth: The Problem Isn’t the People

Senegalese entrepreneur Magatte Wade has built global businesses from Africa. She’s seen the raw talent. The drive. The ideas. The hunger.

Her message?

“Africa isn’t poor because Africans are lazy. It’s poor because the system makes entrepreneurship nearly impossible.”

She calls it “permission-based economies.” In many developing countries, just starting a business requires dozens of licenses, bribes, and approvals — often taking months longer than in the U.S. or Europe.

So even if you’ve got the mindset, you don’t have the infrastructure to win.

🎯 The Bootstrap Narrative Fails Globally

Myth

Reality

“Anyone can invest.”

Not if your currency melts or you can’t access a bank.

“Just learn online.”

Not if you have no internet, no laptop, no electricity.

“Start a business.”

Not if your government makes it illegal or corrupt.

“Just move to a better country.”

Not if your passport locks you out.

🍀 And Yes — Luck Matters More Than We Admit

Even in the U.S., success often comes down to:

Who your parents were

Which zip code you were born in

Whether a policy loophole happened to exist in a year you applied

You may know someone in Haiti who made it to the U.S. only through a temporary rule — and only with personal support. That’s not “bootstrapping.” That’s a rare alignment of chance, help, and timing.

🔑 So What Do We Do?

✅ 1. Stop Pretending Meritocracy Is Global

Effort matters. But effort without access is just exhaustion.

✅ 2. Support Systems That Shrink the Luck Gap

Bitcoin → access to global savings

Online education → access to real skills

Remote work platforms → access to higher wages

Legal reform → access to build freely, without bribery

✅ 3. Build Platforms That Let Value Flow to the Creator

Not to the middleman. Not to the gatekeeper. Not to the “aid industrial complex.” To the person doing the work.

💥 Final Thought

The tragedy isn’t that people in poor countries are lazy. It’s that they’re invisible to the systems that claim to reward merit.

Talent is everywhere. Boots are not.

If we want a fair world, we don’t need more advice. We need to start building the Earned World — where those who create value are finally allowed to keep it.

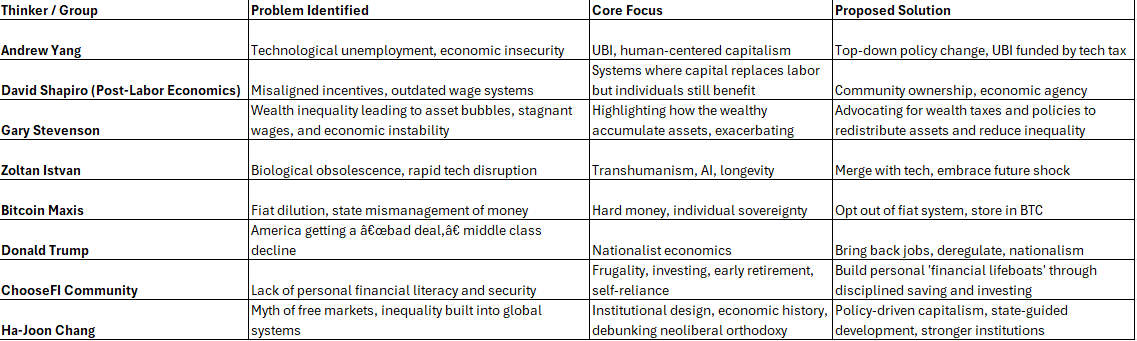

I generated the above table using ChatGPT. I have been invovled in all of these communities that are swirling around the same ideas. I wish I could get them to work together.

ChatGPT also generated the below. It’s not perfect but I wanted to publish it because I want to.

offer it to the world

open for critique and improvements.

The Earned World Manifesto

A Declaration for Builders, Not Rent-Seekers

1. The Problem We See

The current system extracts more than it empowers. It rewards proximity to power, not creation of value. It builds systems that entrench dependency, then calls that stability.

We see:

Productivity rising — but wages stagnating

Knowledge abundant — but credentials gatekept

Labor outsourced — but profit hoarded

Currency inflated — but savings eroded

Talent global — but opportunity gated

Work automated — but ownership concentrated

This is not an accident. The rules are rigged — and the game is extraction.

2. What We Believe

🧱 Agency Is Non-Negotiable

Each individual has the right — and the responsibility — to direct their life. Freedom is not given. It is constructed.

📈 Value Should Flow to the Builder

The person who creates, fixes, or risks should own the upside. Rent-seeking is a tax on the capable.

🧠 Education Must Be Sovereign

Learning is abundant. Gatekeeping it is theft. We reject the credential treadmill in favor of demonstrated skill.

💰 Money Must Be Earned and Preserved

Currency debasement is economic theft. Savings must store effort, not melt it.

🔐 Ownership Is the Foundation

He who owns the tool, the platform, the protocol — holds the power. We choose ownership over permission.

3. What We Support

This is not a utopia. It is a direction.

We support:

🔸 Individuals achieving financial independence through disciplined action

🔸 Workers becoming owners, not just operators

🔸 Monetary systems (like Bitcoin) that cannot be corrupted

🔸 Skill-first pathways over debt-fueled credentials

🔸 Systems that reward contribution, not compliance

🔸 Local or global opt-out zones where new rules can be tested

We reject:

Coerced redistribution

Forced altruism

Dependence disguised as security

4. Our Two-Stage Strategy

🛶 Stage 1: Build your lifeboat. Earn freedom through action. Reduce expenses, save in hard assets, develop durable skills, and reclaim your time.

🏛️ Stage 2: Rebuild the harbor. Use your freedom to build systems that don’t demand sacrifice to survive. Not as charity — but as infrastructure for agency.

5. Join Us

We are the builders. The earners. The ones who won’t rent our future.

We will:

Speak plainly about value and power

Share tools, not just tweets

Reward proof-of-work, not status

Create systems where sovereignty scales

If you’re tired of extraction, If you still believe in ownership, If you’re ready to build —

Welcome to the Earned World.

As I was generating the Manifesto, I had a lot of conversation with ChatGPT. Below was a powerful statement it had.

“The current system extracts more than it empowers.”

This means that the rewards of the modern economy are disproportionately claimed by systems, institutions, and owners — not by the individuals doing the work or taking the risk. The value flows upward, while the burden flows downward.

Here’s what that looks like across different dimensions:

💼 In Work

Wages have stagnated while productivity and corporate profits rise.

Most workers trade time for money with little long-term upside (no ownership, equity, or growth path).

Gig work and contract labor shift costs (insurance, risk, taxes) to the individual while stripping stability.

Extraction: Time, energy, creativity — taken for a wage that doesn’t keep up with cost of living. Empowerment: Would mean building ownership, autonomy, or long-term equity from your work.

💸 In Money

Fiat currency loses purchasing power over time (inflation), punishing savers and wage earners.

Asset inflation (stocks, real estate) benefits those who already hold wealth — not those trying to build it.

Central banks and governments distort money supply in ways individuals cannot control or escape.

Extraction: Your savings melt while those close to the money printer get richer. Empowerment: Would mean access to stable, sovereign, permissionless money, Bitcoin.

🏥 In Healthcare

Healthcare is tied to employment — meaning you’re not truly free to leave your job.

Insurance costs rise faster than wages; many avoid treatment due to fear of bills.

Extraction: Your health and security are used to bind you to jobs and debt. Empowerment: Would mean decoupling basic needs from corporate control.

🏠 In Housing

Real estate is increasingly used as an investment vehicle, not a place to live.

Young people are priced out of ownership, forced into permanent renting.

Extraction: Rent drains wealth every month with no asset built. Empowerment: Would mean pathways to ownership, equity, or cooperative housing.

🎓 In Education

Education costs have exploded, leading to decades-long student debt burdens.

The credential economy keeps people in a treadmill of debt just to be “qualified.”

Extraction: You pay to enter the game, and the game changes by the time you finish. Empowerment: Would mean low-cost, high-agency pathways to skill and livelihood.

🤖 In Technology

Tech companies extract your attention, data, and time to sell to advertisers.

Users create content and community, but ownership and profits go to platforms.

Extraction: You are the product. Empowerment: Would mean open platforms, data sovereignty, and user-owned networks.

🔁 Why This Matters

When a system extracts more than it empowers, it means:

The average person gets poorer in power, even if they get richer in consumption.

Stability, dignity, and control are replaced with dependency and precarity.

People become functionaries, not free agents.

Stagnation in the U.S. and suppression in Mexico are two symptoms of the same disease:

A system where capital moves freely, but labor and ownership do not.

Personal sovereignty is the prerequisite for systemic sovereignty.

Entrepreneurship without savings is economic quicksand.

I think there are solutions to a lot of these propblems. But this is teh start of framing for myself to think more about solutions.

I encourage everyone in the communities I identified to read this as well as consider how they coudl work to make their own lives better as well as make the system better.

I want to highlight the 2 step process.

🛶 Stage 1: Build your lifeboat. Earn freedom through action. Reduce expenses, save in hard assets, develop durable skills, and reclaim your time.

🏛️ Stage 2: Rebuild the harbor. Use your freedom to build systems that don’t demand sacrifice to survive. Not as charity — but as infrastructure for agency.

While I believe everyone is capable of building their lifeboat, it is certainly harder for some than others.

Please comment with any thoughts you have to update this. Please feed this into AI and discuss with it how you might make chagnes to or improve it.

Here are a few resources I referenced when thinking about this.

Over the past couple weeks, I’ve been diving deep into David Shapiro’s Post-Labor Economics lecture series (linked below — all around 40 min). I’ve listened to each one twice, and then used a mix of ChatGPT, Copilot, and Grok to create four 10-point summaries — one per video. Then I asked ChatGPT to synthesize those into a single meta-summary of the core ideas.

Here are the 4 videos. Each about 40 minutes long.

ChatGPT – Here is a 10-bullet-point meta-summary that synthesizes the key themes and insights from all four “Post-Labor Economics” video summaries:

Automation is Inevitable and Transformative: AI and robotics are displacing human labor across all sectors, making wage-based employment increasingly obsolete while simultaneously threatening consumer demand and economic stability.

Economic Agency is the Core Concern: Individuals require labor rights, property ownership, and voting rights to retain agency. As labor rights erode, property rights become the cornerstone of financial autonomy.

The Demand Paradox: Businesses want to automate to cut costs but still need paying customers. Without jobs, people can’t spend—creating a structural contradiction that leads to economic collapse unless resolved.

Rethinking Metrics: The EAI: Traditional KPIs like GDP and unemployment are no longer sufficient. The Economic Agency Index (EAI) measures household income sources (property, wages, transfers) and highlights the need to prioritize ownership income.

UBI: Helpful but Not Enough: Universal Basic Income is necessary as a safety net but inadequate on its own due to inflation risk, governance issues, and centralization. It must be paired with decentralized, property-based income streams.

Ownership is the New Wages: Future economic resilience depends on expanding access to trusts, wealth funds, co-ops, patron equity programs, and digital tokens to replace lost labor income with ownership-based dividends.

Counties as Innovation Labs: With 3,100 U.S. counties, local governments are ideal sites for experimenting with and scaling post-labor economic models, offering granular data and tailored policy solutions.

Banks as Economic Interfaces: Banks will evolve into the primary economic hubs, managing dividend flows, investment portfolios, and identity verification, replacing the role of traditional employers in financial life.

Guardrails Against Technofeudalism: Preventing elite capture and concentrated corporate control is critical. Transparency, participatory governance, and broad-based ownership are essential safeguards.

Market-Driven, Not Ideological: Post-labor economics distinguishes itself from socialism and communism by preserving markets and private property. Its goal is not wealth redistribution through state control, but wealth inclusion through distributed ownership and market-based tools.

I continued to have a conversation with ChatGPT to understand further.

I asked it “”How does post-labor economics differ from individuals simply investing in the stock market to generate passive income?”

It gave a very nicely formatted response, below.

🧩 TL;DR: It’s Not Either/Or

Buying stocks is one tool — a good one — for individual financial freedom.

But post-labor economics is about designing an entire economy where capital income is as normal, widespread, and accessible as having a job once was.

It’s not just you winning the game — it’s everyone getting a seat at the table.

Great question — and an important one.

🤔 At first glance, post-labor economics might sound like:

“Just buy stocks and live off dividends — problem solved.”

But post-labor economics goes beyond that in a few key ways. Here’s how it’s different from individuals simply investing in the stock market:

🏛️ 1. System Design vs. Personal Strategy

Stock investing is an individual solution — you build capital and income for yourself.

Post-labor economics is a system-wide redesign — it’s about building structures where everyone can participate in ownership, even if they don’t have savings, brokerage accounts, or financial literacy.

💵 2. Barriers to Entry

The stock market requires:

Disposable income

Access to financial tools

Risk tolerance

Education

Post-labor models focus on lowering those barriers by:

Distributing residency-based dividends

Creating local trust funds

Offering non-transferable community equity (you don’t have to “buy in”)

🏘️ 3. Ownership of Local, Tangible Assets

The stock market mostly involves ownership of national or global corporations.

Post-labor economics emphasizes ownership of local assets: businesses, land, water rights, data, energy — things that create direct, community-level income streams.

Owning Amazon stock ≠ owning the gas station, solar field, or rental housing in your own town.

🤝 4. Shared Governance & Resilience

When you buy stock, you have no governance power, unless you’re a billionaire activist investor.

Post-labor structures are built on shared governance — resident voting, dividend boards, and community stewardship.

💬 5. Not Everyone Can or Will Invest

A huge portion of the population has no stock market exposure. About 45% of Americans own no equities at all — and among the bottom 50% of income, it’s more like 10–15%.

Post-labor economics seeks to bake ownership into the system so that even non-investors receive income from capital.

🧠 6. Ownership as Policy, Not Privilege

Stock investing is optional and personal.

Post-labor economics treats ownership as infrastructure — like roads or clean water. It should be available to all by design, not just those who planned ahead or got lucky.

🌐 7. Resisting Elite Capture

The stock market concentrates wealth — the top 10% own over 85% of equities.

Post-labor models try to decentralize ownership — giving communities a stake in the economy before everything gets bought up by private equity or mega-corps.

🛠️ 8. Designed for the Age of Automation

Stock market investing was never intended as a wage replacement for the masses.

Post-labor economics is explicitly built to answer:

“What happens when jobs disappear, but people still need income?”

My next question.

“What mechanisms does post-labor economics use to avoid the tragedy of the commons when assets are collectively owned?”

✅ TL;DR:

Post-labor economics avoids the tragedy of the commons by turning shared access into structured, incentivized, accountable co-ownership.

It’s not a free-for-all — it’s a designed economy, where people are rewarded for taking care of what they collectively own.

Excellent question — and one of the core design challenges of post-labor economics.

The tragedy of the commons refers to a situation where a shared resource is overused or neglected because no one feels personal responsibility. In a post-labor economy — where ownership is distributed rather than concentrated — this is a real risk. But it’s not unsolvable.

Here’s how post-labor economics intentionally designs around the tragedy of the commons:

🧩 1. Move from “Common” to “Co-Owned”

The key shift is from open access (commons) to structured, governed co-ownership.

Think: community trusts, resident shares, dividend boards — where everyone has skin in the game, not just access.

📜 2. Define Clear Rights and Responsibilities

Successful post-labor models include smart governance charters:

Who can vote?

Who maintains assets?

How are profits used?

What happens if you leave?

This clarity prevents freeloading and aligns incentives for stewardship.

💰 3. Tie Participation to Rewards

Dividends aren’t just handed out — they can be tied to local contribution:

Show up to meetings

Volunteer hours

Local residency

Use the service or shop locally

This ensures that ownership feels earned, not distant or abstract.

📊 4. Transparency and Dashboards

Many models propose using public dashboards to show how community-owned assets are performing.

When people see the numbers — usage, revenue, maintenance costs — it creates accountability and pride.

🧑🤝🧑 5. Decentralized Governance Structures

Rather than one central authority, post-labor systems push decisions downward:

Counties manage their own trusts

Co-ops elect local boards

Banks help automate compliance and distribution

Local control = stronger stewardship.

🏦 6. Hybrid Ownership Models

Some assets are shared (like land or solar arrays), while others are individually owned (tokens, local equity).

This creates a blended structure where people benefit both as individuals and collectively, reducing the temptation to abuse shared goods.

🛡️ 7. Guardrails Against Elite Capture

Ironically, many “commons” in the modern economy (like housing or water) have already been captured — just not by the public.

Post-labor models bake in protections: voting caps, local-only ownership, anti-speculation rules, etc.

It’s a powerful framework. Personally, I’m still focused on achieving my own financial freedom — and I encourage everyone to do the same. But once we secure our own foundations, we’re in a much better position to help build a freer, more equitable world for everyone.

Introduction In recent years, the corporate world has witnessed a historic shift in treasury strategies, with several prominent companies incorporating Bitcoin into their reserves. Despite these significant changes, many finance professors continue to dismiss or ignore the implications of this trend. During my MBA studies, I have personally discussed or emailed with six finance professors over the last three years about Bitcoin. None of them have shown any curiosity or willingness to engage in meaningful discussions about this topic. While I cannot speak for all finance professors, this has been my experience with those I have interacted with. This paper aims to highlight the lack of intellectual curiosity among academics in the face of obvious transformations in corporate and global environments.

The Corporate Shift to Bitcoin The adoption of Bitcoin by companies such as MicroStrategy, Tesla, and Block Inc. marks a pivotal change in how corporate treasuries manage their assets. These companies view Bitcoin as a strategic asset, providing a hedge against inflation and currency debasement. MicroStrategy, for instance, has aggressively acquired Bitcoin, making it the largest Bitcoin treasury in the world. This trend began around 2020 and has continued to gain traction, signaling a shift in corporate treasury management.

In the last month, several other companies have also announced Bitcoin treasury strategies:

Genius Group: An AI-powered education group that has committed 90% or more of its current and future reserves to be held in Bitcoin 1.

Worksport: A U.S.-based provider of pickup truck solutions that is adding cryptocurrency to its corporate treasury strategy 1.

Rumble: A video platform targeting a conservative audience, planning to invest up to $20 million of surplus cash in Bitcoin 2.

Metaplanet: A company with clearly stated strategy reserve asset goals and reasoning 3.

Strategy (previously MicroStrategy): Continues to lead the way with its Bitcoin treasury strategy 3.

Government Recognition of Bitcoin The U.S. government has also acknowledged the significance of Bitcoin by establishing a Strategic Bitcoin Reserve and a U.S. Digital Asset Stockpile. This move underscores the growing acceptance of Bitcoin as a store of value and its potential role in national economic strategies.

Personal Experience with Academic Dismissal Over the past three years, I have personally discussed or emailed with six finance professors during my MBA studies about the topic of Bitcoin. Despite the clear and significant changes in corporate treasury strategies, none of these professors have shown any curiosity or willingness to engage in meaningful discussions about Bitcoin. This lack of interest is particularly surprising given the relevance of Bitcoin to contemporary financial practices and corporate strategies and the fact that there are not many innovations in Corporate Treasury operations. When a new idea comes along you would expect people to be interested to consider if it has any value.

The Importance of Intellectual Curiosity Intellectual curiosity is a cornerstone of academic excellence. It drives innovation, fosters critical thinking, and encourages the exploration of new ideas. The reluctance of finance professors to engage with the topic of Bitcoin reflects a stagnation in intellectual curiosity that is detrimental to both students and the broader academic community.

Conclusion The corporate shift to Bitcoin represents a significant change in treasury strategies that warrants academic attention. Professors should embrace intellectual curiosity and explore the implications of this trend, rather than dismissing it. By doing so, they can provide students with a comprehensive understanding of the evolving financial landscape and prepare them for the future.

Gary, your crusade against inequality is spot-on—the rich hoard wealth, wages stagnate, and housing slips out of reach. You’ve nailed how the system’s rigged, profiting off disparity as you did at Citibank. But your dismissal of Bitcoin as a “scam” or “musical chairs” misses its point. Let’s break it down through your lens. You see value in what’s tangible—property, bonds, cash flows. Bitcoin’s different: it’s digital scarcity, forged by energy-intensive mining, not free “points on the internet.” It costs real resources—miners burn electricity rivaling small nations to secure it. That’s not hype; that’s a backbone. You’ve said wealth concentration tanks demand, keeping rates low. Bitcoin flips that script. It’s not controlled by banks or governments printing money for the elite—it’s capped at 21 million coins, a hedge against inflation you’ve seen erode workers’ lives. You fear Satoshi’s a shadowy puppetmaster, selling off a million coins to dupe the masses. Check the blockchain—those wallets haven’t moved in 16 years. No secret dump, no conspiracy. Bitcoin’s transparent; anyone can verify it. You’d spot a scam in derivatives a mile away—apply that here. It’s not a rich man’s toy; it’s open to anyone with a phone, from East London to Lagos, leveling a field you know is uneven. You’re right about speculative bubbles, but Bitcoin’s survived crashes—$20K in 2017 to $3K, now thriving in 2025 with institutional buy-in. It’s not about quick riches; it’s a store of value, like digital gold, for a world you’ve seen fail the poor. You’ve bet against broken systems before. Bitcoin’s a bet for one—decentralized, fair, and tough as nails. Give it a trader’s eye, Gary. It’s not the enemy; it’s a tool.

I wanted to share a few quotes from history to highlight that the control and debasement of money by governments has been an issue for a long time. The faster everyone understands this the faster we can all get on the bitcoin standard for value preservation.

I explain here why we should support the bitcoin experiment. It solves the problem. If it ends up failing for some reason in the future, we need to recreate Bitcoin and address whatever issue made it fail because we need a currency that can’t be debased by governments.

“It is utterly clear to me that the highest priority need of world society at the present moment is a realistic economic accounting system which will rectify, for instance, such nonsense as the fact that a top toolmaker in India, the highest paid of all craftsman, gets only as much per month for his work in India as he could earn per day for the same work if he were employed in Detroit, Michigan. – Page 112 Operating Manual For Spaceship Earth, Buckminster Fuller

F.A. Hayek in 1984: “I don’t believe we shall ever have a good money again before we take the thing out of the hands of government, that is, we can’t take it violently out of the hands of government, all we can do is by some sly roundabout way introduce something that they can’t stop.”

“It is well enough that people of the nation do not understand our banking and monetary system, for if they did, I believe there would be a revolution before tomorrow morning.”

“Under the energy currency system the standard would be a certain amount of energy exerted for one hour that would be equal to one dollar. It’s simply a case of thinking and calculating in terms different from those laid down to us by the international banking group to which we have grown so accustomed that we think there is no other desirable standard.”