People often ask me that question when I’m giving a bitcoin presentation or just talking about it one on one. The comparison comes up because Bitcoin is new, people don’t understand it, it has gone up a lot in value, and skeptics assume that must mean someone is being tricked. But to answer it clearly, we need to define what a Ponzi actually is.

A Ponzi scheme is a fraud where early participants are paid “returns” using money from later participants. There’s no productive asset behind it—just cash shuffling from newcomers to old-timers until the inflows slow down and the scheme collapses. Hallmarks of a Ponzi are:

Promised guaranteed returns regardless of the market.

No underlying value creation.

Dependence on new entrants to keep funding old ones.

By that definition, Bitcoin simply doesn’t fit. Bitcoin doesn’t promise anyone a return. It doesn’t pay holders just for owning it. There is no central operator taking money from new buyers to pay old ones. Instead, Bitcoin is an open, neutral monetary network. Its value is set transparently by the market. People buy it because they believe in its properties—scarcity, portability, censorship resistance—not because they’re promised payouts.

Ironically, the system that does mirror a Ponzi structure is Social Security. Today’s workers don’t have their contributions saved for their own retirement. Their payroll taxes are immediately used to pay current retirees. The system only holds up as long as new workers keep entering to fund those already drawing benefits. In other words:

New entrants (workers) pay.

Old entrants (retirees) benefit.

That is the definition of a Ponzi-like structure. And unlike Bitcoin, which can run indefinitely on code and math, Social Security’s days are limited. Demographics are shifting—fewer young workers, more retirees—and that math simply doesn’t work forever. The only thing keeping it afloat today is government borrowing and taxation authority.

👉 Bottom line: Bitcoin is not a Ponzi. It’s voluntary, transparent, and sustainable. Social Security, on the other hand, is the true Ponzi—and its expiration date is nearing!

A common fear I hear about Bitcoin goes something like this: “If it becomes so valuable in the future, people will never spend it. They’ll just hoard it forever — and that means it can’t work as money.”

But let’s pause. That argument assumes that money needs to lose value in order to be useful — that people will only spend if their savings are constantly melting. Does that really make sense?

People Already Save

In reality, people save no matter what. Even with inflationary dollars, households and businesses don’t spend every cent. They put money aside — but because the dollar steadily loses value, they are forced to search for other stores of value:

Stocks

Bonds

Real estate

Gold

Collectibles

This isn’t a feature. It’s a problem. The constant need to escape a leaky dollar creates bubbles, misallocates capital, and makes financial life complicated for everyone.

Take housing, for example. When money loses value, homes become more than shelter — they turn into financial assets. People don’t just buy houses to live in them; they buy them as inflation hedges. That means families looking for a roof over their heads end up competing with investors and savers desperate to preserve wealth. Prices get bid up far beyond the utility value of the home, making affordability worse and turning what should be a basic necessity into a speculative storehouse for capital.

Deflationary Money Doesn’t Paralyze Spending

Critics imagine that if money gains value over time, nobody will use it. But people already spend under deflationary conditions — technology proves this. Everyone knows next year’s phone or TV will be cheaper and better, yet they still buy today. Why? Because they value the use and enjoyment now, not just later.

The same applies to Bitcoin. Once mature, it will likely appreciate at roughly the rate of productivity growth (similar to a low-yield bond). People will hold it to store value — and still spend it when a purchase is worth more than waiting.

Flipping the Narrative

Inflationary money forces people into risky, complex alternatives just to save. Hard money that holds or grows its value removes those distortions. Contrary to the fear, deflationary money won’t break the economy — it may actually fix many of the problems caused by inflationary systems.

And here’s the real irony: many critics already suspect Bitcoin could become extremely valuable — that’s why they worry no one will spend it. But at the same time, they refuse to buy any today. They recognize the upside, but fear keeps them paralyzed on the sidelines.

Conclusion

In a Bitcoin world, homes could go back to being homes, not savings accounts. People could save without speculation, spend without fear of losing purchasing power, and invest in businesses for growth rather than sheltering from inflation. That’s not “useless money.” That’s money finally doing its job.

Disclaimer – If you aren’t comfortable with all potential outcomes, including your Tesla shares dropping 50% in value, you shouldn’t consider this idea.

You also should not consider this if you are unfamiliar with trading options.

I am only sharing this to share information and educate.

I’ve been a Tesla shareholder for years, and I don’t plan to sell my core position anytime soon. But I’ve also been learning about covered calls as a way to generate income at a higher rate than today’s money market funds which currently are paying ~3.5% and going down as rates decrease!. Right now, I see the potential for about a 14% annual yield using this strategy — and I want to take advantage of that while keeping my long-term conviction in Tesla intact.

What’s a Covered Call?

A covered call is one of the simplest options strategies. It works like this:

You own at least 100 shares of a stock. Most options are written where 1 option = a contract for 100 shares.

You sell a call option to someone else, giving them the right (but not the obligation) to buy your shares at a set price (the strike price) by a certain date. For example – “You have the option to buy 100 shares of Tesla from me at $600 on or before 3-20-2026”

You are paid a premium when you sell the option.

Two big things can happen:

If the stock stays below the strike price, the option expires worthless. You keep both the shares and the premium.

If the stock rises above the strike, you may have to sell your shares at that strike price. You still keep the premium, but you miss out on gains beyond that level.

Think of it like renting out your shares — you earn income while you hold them, but you’re capping your upside in exchange.

Why Tesla?

Tesla is currently trading around $440. My existing 400 shares make up about 12–13% of my overall portfolio (roughly $176k out of $1.4M). That’s a meaningful bet, but not my entire net worth. I personally have never looked at options before when I had less money. But I am considering it now with a very small part of my portfolio.

I’ve been holding Tesla for years and plan to continue. I believe in its long-term growth story, Elon Musk’s ability to deliver, and even the possibility of the company eventually reaching an $8 trillion valuation — nearly 6x its current $1.38 trillion market cap. That would potentially happen if Tesla hits all the growth targets in Elon’s proposed new pay package, that is voted on in November 2025. I have already voted yes and hope everyone else does also!

That conviction is what allows me to buy an extra 100 shares — not to hold forever, but to use specifically for covered calls.

The Trade

Underlying: Tesla at ~$440

Shares purchased for strategy: 100 ($44,000)

Option sold: $600 strike, expiring March 2026

Premium collected: ~$30/share = $3,000

The Three Outcomes

Here’s how the trade plays out depending on Tesla’s price by March 20th, 2026:

Scenario

Tesla Price

Outcome

Return

1. Tesla < $440

Falls below my purchase price

Shares drop in value, but I still keep the $3,000 premium. I’ll hold and sell another call in 6 months.

Paper loss on stock, but income cushions downside

2. Tesla $440–$600

Rises but stays under $600

I keep both the shares and the $3,000 premium.

~7% in 6 months (~14% annualized) + stock appreciation

3. Tesla > $600

Blows past $600

Shares are called away at $600. I keep the $3,000 premium plus $16,000 in gains ($160/share).

~$19,000 profit on $44,000 (~43% in 6 months)

How This Fits My Long-Term Tesla Plan

Part of my long-term Tesla strategy for my original 400 shares has always been to gradually divest once it grows too large a percentage of my portfolio — say once it approaches 30–50%.

This covered call approach fits that plan perfectly: it generates income now and gives me a way to get paid while reducing exposure if Tesla keeps climbing.

At $600/share, my portfolio would grow to about $1.5M, and Tesla would represent ~$300k of that (~20%). If 100 shares are called away, I’d reduce Tesla to 400 shares ($240k), which still leaves me with significant exposure.

At $800/share, my portfolio could be around $1.6M. Selling another 100 shares would leave me with 300 shares worth $240k — still ~15% of my portfolio, almost the same weighting Tesla holds today (~12.6%). This is assuming the rest of my portfolio doesn’t also rise. It likely would so really Tesla would end up an even smaller percentage of my portfolio.

So even as I trim, Tesla stays a core but not outsized piece of my investments.

The Long-Term Upside

At $800/share, Tesla would be about a $2.5 trillion company. Even if I’m down to 300 shares at that point, that’s still $240k invested.

And if Tesla grows to an $8 trillion valuation as some expect — a 3.2x increase from $2.5T — my 300 shares could climb to about $768k.

That means even after trimming, I’d still capture massive upside if Tesla’s long-term growth story plays out.

Why This Works for Me

It’s a small slice of my overall portfolio. At ~$44,000, the covered call sleeve is just 3% of my total assets. That makes it a safe experiment that doesn’t threaten my financial foundation.

My core Tesla is protected. My long-term 400 shares are untouchable. The 100 new shares are my “income Tesla” — designed to work harder without risking my conviction stake.

All three outcomes are acceptable. If Tesla dips, I’ll just sell another call. If it grinds sideways, I pocket income. If it rips higher, I still earn a great return, even if I give up some upside.

It aligns with my long-term plan. Selling calls is a structured way to generate income and gradually reduce Tesla’s weight in my portfolio as it grows.

Conviction makes it possible. I’m comfortable capping the upside on 100 shares because I still own 400 more shares that will fully benefit if Tesla continues to grow. This way, I get income from a small slice of my position, while my larger core holding remains positioned for the long-term upside.

Testing My Future Retirement Plan

This trade is also a trial run for my early retirement plan. If I eventually trim my Tesla position to around $240k (say 300 shares at $800), I could use the same covered call strategy to generate income.

At ~14% annualized, that $240k could potentially produce about $33k per year in income — without me ever touching the rest of my portfolio.

That’s a powerful idea: one high-conviction stock position, managed carefully with covered calls, could provide a meaningful cash flow stream in retirement while my index fund base continues to compound.

My Investing Context

Most of my portfolio is in index funds. That’s my base strategy — low-cost, diversified, and reliable.

But Tesla (and Bitcoin) are my two exceptions. I’ve listened to years of Tesla content, followed the company’s progress, and watched Elon Musk repeatedly deliver on ambitious goals. I believe in the growth story.

Final Thoughts

Covered calls aren’t “free money.” They limit your upside, and they only work if you’re comfortable with all possible outcomes. For me, splitting my Tesla into two buckets — 400 shares conviction hold, 100 shares income strategy — strikes the right balance.

Tesla remains my long-term hold. The extra 100 shares are simply there to spin off cash flow, provide income, and help me get paid while gradually divesting. That way, Tesla stays a meaningful but balanced piece of my portfolio — while still giving me the chance to benefit if Elon Musk delivers on the $8 trillion vision.

And looking ahead, this strategy doubles as a test run for retirement income — showing how one well-managed conviction position can help fund financial independence.

If you aren’t comfortable with all potential outcomes, including your Tesla shares dropping 50% in value, you shouldn’t consider this idea.

You also should not consider this if you are unfamiliar with trading options.

I am only sharing this to share information and educate.

Money market funds have quietly become a $7.7 trillion behemoth. They’re the go-to “safe yield” for investors and savers alike. But with the Federal Reserve now in an easing cycle, those yields — currently around 3.5%–4% — are headed lower.

That’s where Strategy’s Bitcoin-backed perpetual preferreds come in. While most people know Strategy (MSTR) as the largest corporate holder of Bitcoin, fewer realize that it has built a full yield curve of preferred instruments, each engineered for different investors.

Where These Instruments Sit in the Capital Stack

Most senior → Debt (convertible notes) → STRF (Strife) → STRC (Stretch) → STRK (Strike) → STRD (Stride) → Common (MSTR) → most junior / volatile.

The Rationale: Building a Bitcoin Yield Curve

STRF (Strife): Senior, cumulative, fixed dividend, long-duration. Currently yielding about 9%.

STRC (Stretch): Senior to STRD and STRK. Variable monthly dividend, engineered to trade around $99–$101, currently yielding about 10.25%.

STRK (Strike): Convertible hybrid with both dividend and equity-conversion features. Not my focus here, but it’s an important part of the structure.

STRD (Stride): Junior high-yield, fixed 10% dividend, currently yielding about 12.7% due to market pricing in more perceived risk. Functionally similar to STRF, except dividends are non-cumulative (can technically be skipped). That said, I believe skipping would be highly unlikely, as it would damage trust and Strategy’s ability to raise future capital. Dividends are paid quarterly.

Visualizing the Yields

Here’s how these instruments compare against traditional money markets:

Money Market (green): conservative baseline at ~3.5–4%.

STRF (orange): senior, stable preferred with ~9%.

STRC (orange): short, steady instrument at ~10.25%, engineered to trade near $100.

STRD (orange): dynamic junior instrument at ~12.7%.

Why I Prefer STRC and STRD

I’m drawn most to STRC and STRD.

STRC is designed to be the least volatile of the group, with a monthly payout and mechanisms (ATM issuance, variable rate, call option) that help stabilize its price.

STRD is the high-yield gear, juiced by its junior position in the stack. While the market demands extra yield for perceived risk, I personally think that risk is overstated given Strategy’s Bitcoin reserves and incentives to maintain dividend trust.

Together, they cover two ends of the spectrum: steady monthly yield vs. higher-octane quarterly yield.

A Practical Emergency Fund Example

Suppose you have a $10,000 emergency fund.

All in Money Market: $10,000 × 4% ≈ $400/year.

Blend with STRC: Keep $7,500 in money markets (=$300/year) and put $2,500 into STRC (=$256/year).

Total = $556/year — a 39% boost without overcommitting.

I wouldn’t put my entire emergency fund into a new instrument like STRC — safety and liquidity should come first. But even a modest allocation can noticeably lift your yield while still keeping most reserves conservative.

Closing Thought

Strategy is essentially pioneering a new financial system built on Bitcoin collateral. If they can consistently pay these dividends — even through Bitcoin downturns — it would be revolutionary. It would prove that Bitcoin isn’t just “digital gold,” but the foundation for a new class of yield-bearing, creditworthy instruments.

Here are 2 videos of when STRC and STRD were initially offered. They offer a lot of information about how these work.

Bitcoin, Deflation, and the Myth of “Useless Money”

A common fear I hear about Bitcoin goes something like this: “If it becomes so valuable in the future, people will never spend it. They’ll just hoard it forever — and that means it can’t work as money.”

But let’s pause. That argument assumes that money needs to lose value in order to be useful — that people will only spend if their savings are constantly melting. Does that really make sense?

People Already Save

In reality, people save no matter what. Even with inflationary dollars, households and businesses don’t spend every cent. They put money aside — but because the dollar steadily loses value, they are forced to search for other stores of value:

Stocks

Bonds

Real estate

Gold

Collectibles

This isn’t a feature. It’s a problem. The constant need to escape a leaky dollar creates bubbles, misallocates capital, and makes financial life complicated for everyone.

Take housing, for example. When money loses value, homes become more than shelter — they turn into financial assets. People don’t just buy houses to live in them; they buy them as inflation hedges. That means families looking for a roof over their heads end up competing with investors and savers desperate to preserve wealth. Prices get bid up far beyond the utility value of the home, making affordability worse and turning what should be a basic necessity into a speculative storehouse for capital.

Deflationary Money Doesn’t Paralyze Spending

Critics imagine that if money gains value over time, nobody will use it. But people already spend under deflationary conditions — technology proves this. Everyone knows next year’s phone or TV will be cheaper and better, yet they still buy today. Why? Because they value the use and enjoyment now, not just later.

The same applies to Bitcoin. Once mature, it will likely appreciate at roughly the rate of productivity growth (similar to a low-yield bond). People will hold it to store value — and still spend it when a purchase is worth more than waiting.

Flipping the Narrative

Inflationary money forces people into risky, complex alternatives just to save. Hard money that holds or grows its value removes those distortions. Contrary to the fear, deflationary money won’t break the economy — it may actually fix many of the problems caused by inflationary systems.

And here’s the real irony: many critics already suspect Bitcoin could become extremely valuable — that’s why they worry no one will spend it. But at the same time, they refuse to buy any today. They recognize the upside, but fear keeps them paralyzed on the sidelines.

Conclusion

In a Bitcoin world, homes could go back to being homes, not savings accounts. People could save without speculation, spend without fear of losing purchasing power, and invest in businesses for growth rather than sheltering from inflation. That’s not “useless money.” That’s money finally doing its job.

Most people don’t realize that many of the economic problems facing Americans today trace back to something called the Triffin dilemma. Politicians like Trump rage about trade deficits or promise to bring back jobs, but they rarely understand the underlying monetary system that makes those promises impossible to keep. And because they don’t understand it, millions of middle-aged workers in the U.S. are left angry and disillusioned.

But here’s the good news: the problem is solvable. And Bitcoin, combined with Buckminster Fuller’s vision of a “world accounting system,” offers a way forward.

The Triffin Dilemma in Plain English

Robert Triffin pointed out a paradox in the 1960s: if one country’s currency becomes the world’s reserve currency, that country must constantly supply it to the rest of the world. For the U.S., that means running trade deficits and flooding the globe with dollars.

The catch is that what looks good globally causes pain domestically. To meet the world’s demand for dollars, the U.S. must run deficits, borrow more, and tolerate an overvalued dollar. That makes American exports less competitive, hollows out manufacturing, and weakens wage growth.

The Cost of Supplying the World with Dollars

To keep the global economy running on dollars, the U.S. has to keep sending them out. There are only two main ways that happens: by running trade deficits (importing more than we export) or by borrowing (issuing Treasuries that foreigners buy with their surplus dollars). Both of these mechanisms keep the world awash in dollar liquidity — but they impose heavy costs on American workers.

Persistent deficits mean more borrowing. Every trade deficit eventually gets financed with U.S. debt. Foreign governments and investors recycle the dollars they earn back into U.S. Treasuries. The system keeps spinning, but America’s national debt climbs ever higher.

Global demand keeps the dollar strong. Because the world needs dollars, our currency stays overvalued compared to others. A strong dollar makes imports cheap (which feels good for consumers at Walmart) but makes American exports expensive (which is brutal for manufacturers trying to compete abroad).

Manufacturing gets hollowed out. When American goods are too expensive, factories lose business. Over time, companies either shut down or relocate production overseas. Entire industries migrate abroad, leaving behind shuttered plants and devastated communities.

Take steel as a concrete example. In the late 20th century, global demand for dollars, combined with cheaper steel production in Asia, kept the U.S. dollar strong and U.S. steel prices uncompetitive. By the 1980s and 1990s, iconic steel towns in Pennsylvania and Ohio watched mills close. Workers who once earned solid middle-class wages saw their jobs vanish, and many never found work at the same pay level again.

Wages stagnate. With fewer competitive industries at home, American workers lose bargaining power. They’re forced to compete against cheaper labor abroad, and wage growth flatlines. Meanwhile, the cost of living — housing, healthcare, education — keeps climbing. The result is the frustration many middle-aged Americans feel today: they’ve worked hard their whole lives, yet the system seems rigged against them.

In short: to supply the world with dollars, America borrows, tolerates an overvalued currency, and sacrifices its own competitiveness. The global dollar system helps keep international trade flowing, but it extracts its pound of flesh from U.S. workers.

Figure 1: Global demand for dollars keeps the dollar strong, which makes imports cheap but exports uncompetitive — hollowing out U.S. manufacturing and holding down wages.

Why Trump (and Most Politicians) Miss the Point

Trump recognizes that something is broken — but his diagnosis is shallow. He blames foreign countries, bad trade deals, and weak leaders. His answer is tariffs and protectionism.

But the deeper issue is that America can’t stop running deficits without undermining the very system that makes the dollar the global reserve. The Triffin dilemma locks us in. Protectionism only papers over the problem temporarily.

How Wages Would “Automatically Adjust” Under Bitcoin

Now imagine a world where global trade is denominated in Bitcoin, a money no government can print or devalue.

High Productivity Raises Wages Locally If Country A is extremely productive, it earns more Bitcoin. Workers there see higher wages in BTC terms.

Prices Rise in the Productive Country With higher wages, local goods get more expensive relative to other countries.

Trade Shifts Other countries stop buying from Country A and look to Country B or C, where wages are lower and goods are cheaper.

Jobs Move, Wages Rebalance Jobs flow out of the high-wage country into lower-wage ones. Wages in the expensive country stabilize or even fall, while wages in cheaper countries rise.

The result: wages “automatically” adjust across borders to reflect real productivity, not the games governments play with currency printing or manipulation.

Figure 2: Under a Bitcoin-based system, wages and trade flows automatically rebalance. High wages make exports more expensive, shifting jobs abroad until global wages reflect true productivity.

Why Fiat Prevents This Natural Balance

In today’s fiat system, governments intervene to block this natural adjustment. They devalue their currencies to keep exports cheap, trapping workers in low wages and preventing global wage convergence.

Meanwhile, American workers face the opposite problem: a strong dollar that prices them out of global competition. The Triffin dilemma ensures the imbalance persists.

“Isn’t It Just Greedy Companies Suppressing Wages?”

A common belief is that big U.S. companies are the real villains — trillion-dollar firms posting record profits while holding wages flat, outsourcing jobs, or using H1B visas to bring in cheaper labor. There’s truth in that frustration, and yes, there is abuse in how the visa system is used.

Consider this example: if an American worker expects $80,000 but a skilled H1B worker is willing to accept $50,000, the company has a clear incentive to hire the cheaper worker. To Americans, this feels like wage suppression. But for the H1B worker, it’s a huge win. That $50,000 U.S. salary might translate into the equivalent of $150,000 back home, especially if they can send $10,000 to family abroad where the cost of living is far lower.

So while it looks like companies are simply greedy, they’re really responding to the incentives of a distorted global money system. With the dollar overvalued and global trade imbalances baked in, U.S. labor is structurally overpriced compared to the rest of the world. Companies are not the root cause — they’re just playing the game according to the rules we’ve set.

In a Bitcoin-based system, the game changes. Wages would adjust across borders automatically, not through currency manipulation or immigration loopholes. Companies would still seek efficiency, but the playing field would be leveled: wages in every country would reflect true productivity, not fiat distortions.

Figure 3: Under fiat money, companies are incentivized to outsource, use H1B labor, and suppress wages. Under Bitcoin, wages converge globally based on real productivity, not manipulated exchange rates.

Fuller’s Dream of a World Accounting System

Buckminster Fuller envisioned a future where humanity had a scientific, global accounting system that measured real wealth and resources instead of manipulating national ledgers.

Bitcoin is a step in that direction. It’s transparent, borderless, and immune to political distortion. A Bitcoin-based world economy would essentially run on Fuller’s “world accounting system,” with wages, trade, and prices reflecting true productivity instead of central bank policy.

The Takeaway

The middle-aged frustration in America isn’t just about lost jobs or bad politicians. It’s about being trapped inside the Triffin dilemma — a system where the U.S. must sacrifice its workers to supply the world with dollars.

Bitcoin offers a way out: a neutral, global money where wages naturally rebalance, trade adjusts fairly, and no single country bears the impossible burden of being the world’s reserve.

It’s not just a monetary upgrade — it’s the foundation for a more honest accounting system for the entire world.

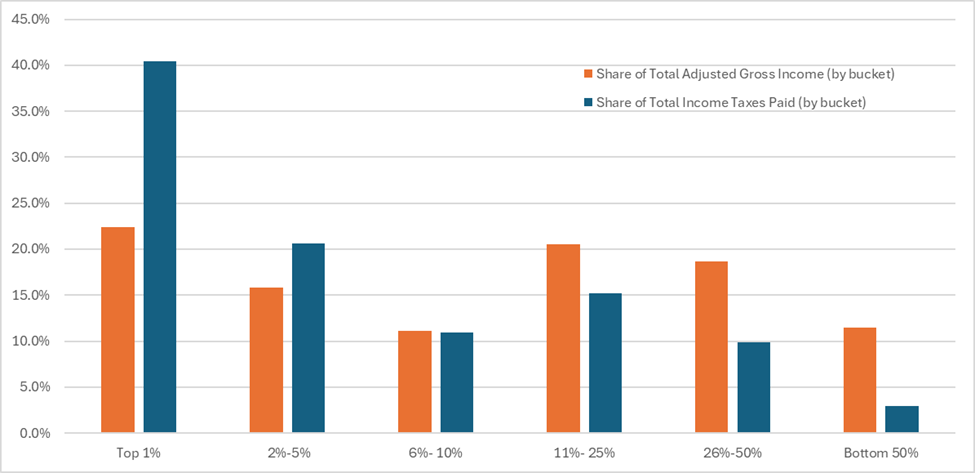

When we talk about taxes in America, the debate often gets sloppy. People use “income” and “wealth” almost interchangeably, but they’re very different things.

Income is the flow of money earned each year — wages from a job, dividends, or realized capital gains.

Wealth is the stock of assets someone already owns — businesses, real estate, stocks, Bitcoin, etc.

Our tax system is built mainly on income, not wealth. And when commentators conflate the two, it clouds the conversation about fairness and policy.

Income Snapshot

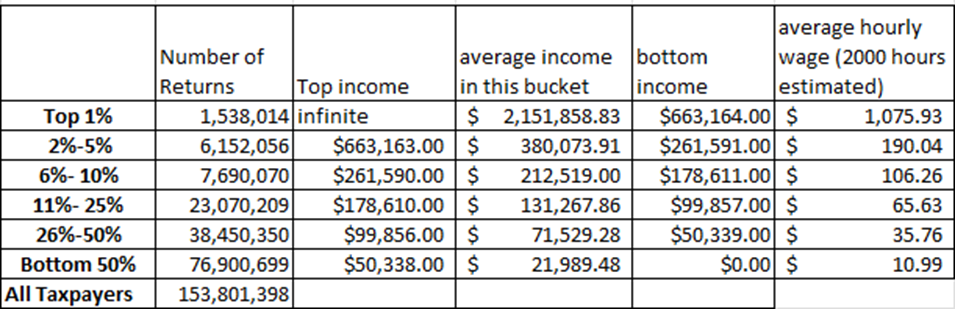

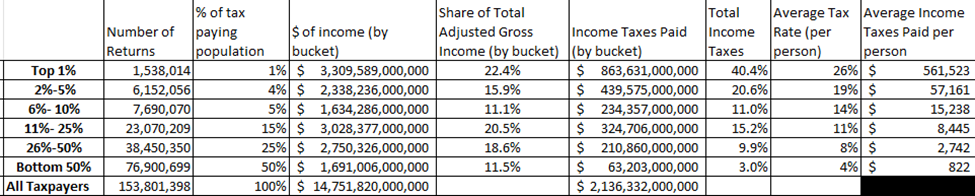

In 2022, the U.S. collected $2.1 trillion in federal income taxes on about $14.8 trillion in total income. That’s about 14.4% of taxable income.

Divide that income across all 153 million taxpayers, and the average income comes out to $95,915, or about $47.96 per hour assuming 2,000 hours of work per year. Of course, averages can mislead — the distribution is anything but equal.

The Top 1%

To qualify for the top 1% in 2022, you needed at least $663,164 of income. On average, these 1.5 million taxpayers earned $2.1 million each.

Share of income: 22.4%

Share of taxes paid: 40.4%

Effective tax rate: 26%

The Bottom 50%

The bottom half — about 76 million taxpayers — earned less than $50,339 per year. Their average income was just $21,000, totaling $1.7 trillion across the group.

Effective tax rate: ~4%

Many pay no federal income tax at all, often due to credits like the Earned Income Tax Credit (EITC) or child tax credits.

Wealth Snapshot

If we shift from income to wealth, the picture looks even starker. As of mid-2025, U.S. billionaires hold over $6.2 trillion in wealth, spread across only about 813–867 individuals.

But here’s the catch: the U.S. government is adding about $2 trillion in deficit spending every year. Even if you taxed billionaires at extremely high rates, it might cover only a year or two of deficits. After that, the wealth pool would shrink — and most billionaires would likely relocate to avoid such aggressive taxation.

That doesn’t mean we shouldn’t debate fairness, redistribution, or even wealth taxes. But it does mean we need to be realistic about the math.

Why This Matters

The key takeaway is that income and wealth are different conversations. Most tax debates focus on income flows, yet the loudest arguments are often about wealth concentration. If we mix those together, we miss the real tradeoffs.

I’m happy to debate how much each group should earn, or whether a wealth tax makes sense (though I personally think it doesn’t). But if we want an honest conversation, we have to separate what we’re actually measuring.

Because when we ask, “Who should pay more?” the first step is being clear: are we talking about annual income, or about the stock of wealth built up over decades?

You will notice myd ata is slightly different than from the website. The website continually aggregates so their “top 5%” data includes all the income & people from the top 1% + the 2%-5%. I have broken it down so you can see how much income is in each bucket. I think my method is much more useful. It also allows you to see how much income, taxes, average income, is in each bucket.

When the data is aggregated it always is skewed due to the higher amount of income above it.

Bitcoin doesn’t need you. But maybe—just maybe—you need Bitcoin.

Every cycle, new people show up thinking they’ve discovered something revolutionary—whether it’s questioning Bitcoin’s energy use, proposing faster payment layers, or trying to “fix” volatility. But every idea you’ve had about Bitcoin… has already been debated, attacked, memed, improved, or discarded years ago. The Bitcoin rabbit hole is deep, and it’s been dug for over 15 years by some of the most paranoid, visionary, and relentless minds on the planet.

Bitcoin isn’t some niche internet plaything anymore. It’s now held on balance sheets, integrated into national energy grids, and embedded in the financial strategies of countries and corporations alike. And yet, most people still ignore it—until they can’t.

How long can you ignore a monetary network that’s eating inflation, resisting censorship, and refusing to die?

Bitcoin doesn’t wait. It doesn’t care if you “believe” in it. It just keeps producing blocks every 10 minutes, no matter what. The longer you delay engaging with it, the more ground you lose—not just financially, but intellectually. Because by the time you show up with your “fresh” take, there’s already a thousand-page thread archived on Bitcointalk dismantling it.

Bitcoin doesn’t need you. But maybe—just maybe—you need Bitcoin.

🧠 Common Questions (Yes, They’ve Already Been Answered)

Before you leave a comment or dismiss Bitcoin entirely, check below—your question has probably been asked, answered, and refined for years. But if it hasn’t, ask! The Bitcoin rabbit hole only gets deeper when you engage.

Drop them in the comments or send me a message—I’m always open to honest discussion. But I strongly encourage you to do a little digging first. Chances are, someone’s already asked your exact question… and the answer is better than you’d expect.

Bitcoin is not just about beating inflation or outperforming Wall Street. It’s about dignity. It’s about sovereignty. It’s about creating a world where value can’t be stolen.

So the next time someone asks what Bitcoin is, tell them this:

It’s not an investment. It’s a revolution.

Why the youth are turning to math instead of politicians to fix what was broken before they were born.

“If we could just print money, why is there poverty, war, and hunger?” — Jack Mallers

👋 Jack Mallers Is Saying What I’ve Been Trying to Say

Every once in a while, someone steps up and articulates your beliefs more clearly, more passionately, and more publicly than you could yourself.

That’s what Jack Mallers did in his recent keynote. He didn’t just explain Bitcoin — he captured the emotional, moral, and generational reasons I’ve written about on my blog:

We aren’t just investing in Bitcoin. We’re opting out of a broken system. We’re building something better.

This summary breaks down his talk. It’s one of the clearest cases I’ve seen for Bitcoin as a moral revolution, not a financial asset.

🧠 Mallers’ Core Thesis: Bitcoin Is a Moral Revolution

Not a speculative asset. Not a tech fad. Not a hedge fund toy.

🧨 Bitcoin is an ethical, generational response to a broken fiat system that’s hollowed out society.

🚨 A Generation in Crisis

Millennials and Gen Z were told to go to college — and walked away with six-figure debt. We were told the economy is booming — while we’re priced out of homes. We were told to “just work hard” — while real wages stagnate and healthcare bankrupts families.

Petrodollar (1974): The dollar’s global dominance is enforced by oil deals and military might.

The U.S. prints money. The world ships us real goods. We don’t produce — we consume. We don’t export labor — we export inflation, instability, and war.

“Fiat currency is a moral violation,” Mallers says. “It’s time travel. You’re spending your kids’ future without their consent.”

⚖️ The Triffin Dilemma: Why the Middle Class Had to Die

Economist Robert Triffin warned that a nation with the global reserve currency must choose between:

Domestic stability

Global demand

America chose global demand.

The result? We shipped jobs overseas. We poisoned our food. We hollowed out our towns and our families. We replaced meaningful work with dependency — then blamed the poor for being poor.

And it was on purpose.

“They knew,” Mallers reminds us. “This wasn’t an accident. It was the cost of empire.”

⚰️ 50 Years of Consequences

Mallers lays it out plainly: when you debase money, you debase everything else.

📉 Wages stagnated while assets inflated.

🍔 Diets worsened as processed food replaced real nutrition.

💊 Mental health and family formation collapsed.

🧱 Hard work stopped paying off.

“All of this started in 1971,” he says again and again. “That’s weird, isn’t it?”

🔐 Bitcoin: A Peaceful Revolution Built on Math

Against this backdrop, Bitcoin isn’t just a shiny asset — it’s a moral tool.

It’s a response to a system built on theft, control, and decay.

Bitcoin’s moral code:

You shall not inflate.

You shall not confiscate.

You shall not censor.

You shall not counterfeit.

Unlike fiat, Bitcoin is enforced by math, not military. Private keys are stronger than guns. You can steal a house. You can loot a bank. But you can’t steal 256-bit encryption locked in someone’s mind.

“Bitcoiners are Bitcoin,” Mallers says. “Before it’s a network, it’s a movement. Before it’s code, it’s ethics.”

💡 The Future Isn’t Given — It’s Built

We didn’t ask for this system. We didn’t choose to be born into debt and decay. But we get to choose what comes next.

Bitcoin is the latest chapter in the story of human innovation. Like fire, the printing press, the computer — it’s a tool to reclaim our agency. It lets us opt out of a system that exploits us and build one based on fairness and freedom.

“After you wipe your last tear,” Mallers asks, “what do you want to do?”

🎯 Final Word: Choose Ethical Money

Bitcoin is not just about beating inflation or outperforming Wall Street. It’s about dignity. It’s about sovereignty. It’s about creating a world where value can’t be stolen.

So the next time someone asks what Bitcoin is, tell them this: