Earlier in 2024, I read a local article about Washington’s senior senator proudly announcing how much federal money she had brought home to the state. Her list ran dozens of pages — hundreds of millions in Congressionally Directed Spending, better known as earmarks.

She’s not alone. Nearly every senator submits earmark requests, which you can browse on the Senate Appropriations Committee’s official list. Each item sounds worthy enough: a wastewater upgrade, a community arts incubator, a “therapeutic court.” But taken together, these line items add up fast.

According to the Peter G. Peterson Foundation, Congress approved 8,098 earmark projects costing $14.6 billion in FY 2024—about the same as FY 2023—and still under one percent of total discretionary spending. In context, that’s roughly 0.2 percent of total federal outlays.

It’s easy to shrug and say, “So what? That’s peanuts in a $6.8 trillion budget.”

But the issue isn’t the size. It’s the signal.

The Round-Trip Problem

When money takes the round trip — federal tax → congressional politics → earmark → local grantee — it leaks. Every stop adds overhead, lobbying, and political friction.

If a project’s benefits are local, fund it locally. Save federal dollars for truly national needs—and make any remaining federal grants competitive and audited.

That’s not ideological; it’s basic hygiene. Less leakage, less pork, more accountability.

The GAO’s Quiet Crusade

The Government Accountability Office (GAO) has spent over a decade documenting federal overlap, duplication, and inefficiency. Between 2011 and 2023, its recommendations produced about $667 billion in cumulative savings—roughly $51 billion a year.

That sounds impressive… until you set it beside annual deficits averaging $1.2 trillion over the same period. Even if every GAO fix were implemented perfectly, it would only offset a few cents of every deficit dollar. We celebrate small wins while ignoring the structural math.

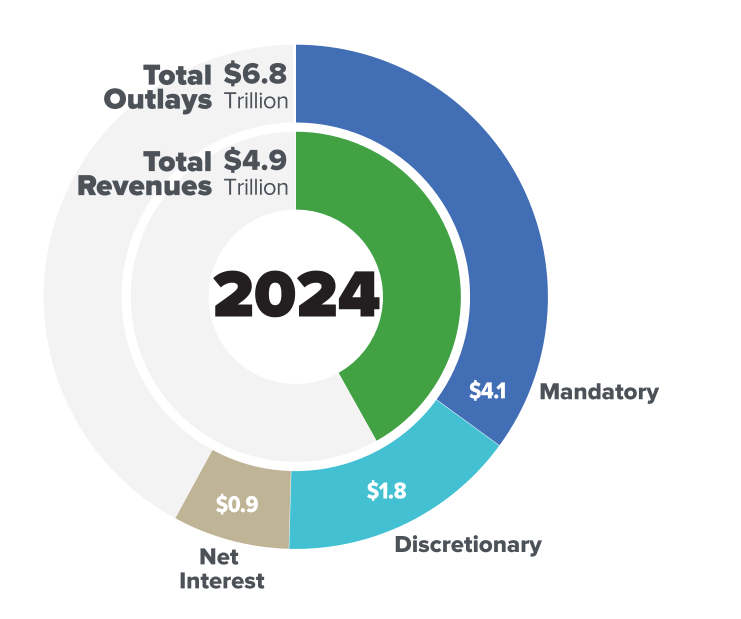

The Trillions That Run on Autopilot

To understand that math, look at the 2024 federal budget as a whole (data from the Congressional Budget Office’s Budget and Economic Outlook: 2024–2034):

- Total Outlays (FY 2024): ≈ $6.8 trillion

- Total Revenues: ≈ $4.9 trillion

- Mandatory Spending: ≈ $4.1 trillion (60%) — Social Security, Medicare, Medicaid, and other entitlements

- Discretionary Spending: ≈ $1.8 trillion (26%) — defense, education, housing, infrastructure, research

- Net Interest: ≈ $0.9 trillion (13%) — the fastest-growing line item in the budget

Source: Congressional Budget Office, “Budget and Economic Outlook: 2024–2034.”

All the fights over earmarks, audits, and waste reports happen inside that discretionary slice, the part Congress actually votes on each year.

The other 70 percent runs on autopilot — driven by demographics, healthcare inflation, and debt.

So yes, we have a trillions problem, not a billions problem.

But pretending the billions don’t matter ensures the trillions never get fixed.

The Cultural Incentive to Spend

Politicians are rewarded for bringing money home. A senator who resists earmarks looks “ineffective.”

That same incentive—spend now, borrow later—is what prevents any real reform on the mandatory side.

If Congress can’t resist handing out $14 billion in earmarks to score headlines, how will it ever take on the hard reforms that actually matter?

The Real Problem

The problem isn’t that earmarks alone bankrupt the country — they don’t.

The problem is that they reveal a mindset: Washington still rewards politicians for spending, not stewardship.

Every senator gets praised for what they bring home, not for what they turn down.

That’s the same mindset that makes real entitlement reform politically impossible and deficit reduction unthinkable.

Earmarks aren’t bankrupting the U.S., but they show why the U.S. can’t stop bankrupting itself.

Until that incentive changes — in Congress, in media, and among voters — the numbers will keep getting bigger, and the excuses will too.

✅ Sources:

- Sen. Patty Murray press release (March 2024)

- Senate Appropriations Committee — FY 2024 CDS chart

- Peter G. Peterson Foundation: What Are Earmarks? (2024)

- GAO 2024 Annual Report on Fragmentation, Overlap, and Duplication

- CBO Budget and Economic Outlook: 2024–2034

- Requested by only one chamber of Congress;

- Not specifically authorized;

- Not competitively awarded;

- Not requested by the President;

- Greatly exceeds the President’s budget request or the previous year’s funding;

- Not the subject of congressional hearings; or,

- Serves only a local or special interest.